Following the raft of legislative and regulatory roll-outs in recent years, buy-to-let’s ongoing transformation looks set to trigger an exodus of highly-geared landlords in the coming years. Some also predict that the sector’s overall attractiveness as an asset class amongst retail investors may also dissipate.

Nonetheless, for the majority that choose to remain, and perhaps even astutely capitalise on this new operational environment, a robust financial plan to protect current and future holdings will be a must.

Therefore, in addition to effective tax planning, cost management and other strategies to buffer against the inevitable market turbulence, understanding how to access cost-effective mortgage finance is of paramount importance.

In this post, we outline some of the factors that contribute to how mortgages and remortgages against buy-to-let properties are underwritten – which we hope you can apply on a more practical level to secure the best deals possible.

Please click on the hyperlinks in the content box below to access each section, and on the arrow on the right to scroll back to the top of the post.

Mortgage Lender Risk Averseness (Macro)

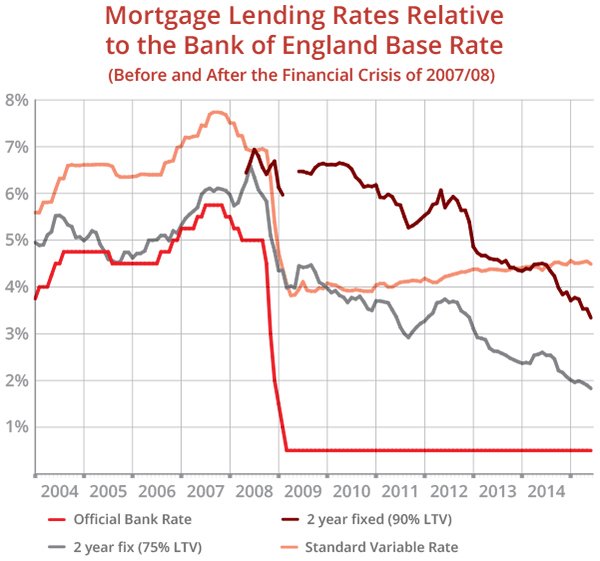

The Bank of England Base Rate (BBR), as established by the Monetary Policy Committee (MPC) monthly meetings, is arguably the most commonly recognised influence on the mortgage market – having a direct effect on tracker, discounted and standard variable / revert rates across the board.

However, it would be incorrect to assume that rises and falls in the BBR directly correlate to what you can expect to be charged as a borrower.

All mortgage lenders continually monitor their own business models and margins. The graph below, for example, demonstrates how it took some years for commercial rates to drop in the aftermath of the financial crisis – despite the historically low base rates since 2009. This was largely due to the uncertainty surrounding the future of the property market alongside what were then unknown impacts of government-led bailouts.

As funding conditions improved, confidence was restored and the number of lenders entering or re-entering the arena increased – thereby creating a healthier environment for more competitive mortgage rates.

These trends tend to demonstrate that, in addition to the specific risks inherent to the buy-to-let sector itself, lenders will pay close attention to a wide range of economic factors, political decision-making and property cycle positioning. Therefore – in the coming years – everything from Brexit, Sterling’s value and its influence on inflation to unemployment / underemployment, consumer confidence, stock market performance, infrastructure investment and spending priorities should all be observed closely.

Essentially, where there are any indications that the economy may be moving into negative territory, the possibility of borrower default goes up. At these times, it would therefore make more sense for lenders to take a more risk averse approach to their internal underwriting processes.

The Yield Curve

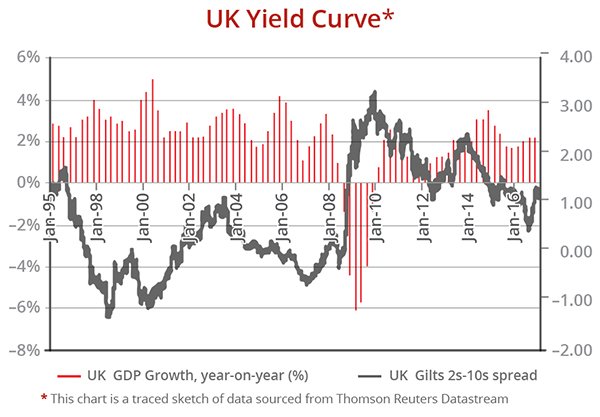

Yield curves plot the return levels of relatively stable fixed-income investments such as government bonds (gilts) across various time periods, or maturities. Mortgage lenders look at how the gradient of the slope evolves over time and broadly draw upon the following suppositions:

- A steepening yield curve: where long-term gilt yields are higher than short-term gilt yields. This is typically an indication of stronger economic growth and inflation, resulting in the increased likelihood of rising interest rates;

- A flattening yield curve: where long-term gilt yields begin to stagnate. The market may anticipate an economic slowdown and, potentially, a decrease in interest rates;

- An inverting yield curve: where the long-term gilt yields are lower than short-term bond yields, reflecting an economic downturn and ensuing interest rate cuts.

Argued to be the best barometer of ongoing central bank monetary policy, the “2s10s curve” references the yield relationship between 2 and 10-year gilts. The graph below plots the UK spread from January 1996 until shortly after the Brexit decision in June 2016:

Appreciating that the shape of the yield curve is influenced by a range of granular factors, there are some more general trends that can be observed from recent history. The inverted contour towards the latter half of the 1990s, for example, was largely reflective of the Asian debt crisis. A few years later, a steepening trend during the Blair-Brown “boom” years was seen; then a flattening / inverting curve prior to a more noticeable invert before and during the financial crisis (when interest rates were dropped to historical lows). As quantitative easing, low-interest rate policies and other stimulus mechanisms were deployed to avoid a depression, the curve began to steepen sharply. This was then followed by a series of peaks and troughs as the economy recovered. Towards the right of the graph, there was also a brief invert as markets panicked in response to the EU referendum result.

London Inter-Bank Offered Rate (LIBOR) for Buy-to-Let Investors

In order to raise their own levels of liquidity, banking institutions frequently borrow through savers, wholesale markets, mortgage-backed securities and from other banks.

Calculated on a week daily basis, the London Inter-Bank Offered Rate (LIBOR) can be defined as the average costs that banks borrow from each other for short-term loans. Informally referred to as the “substructure” for actual lending rates, the LIBOR is used as a reference to price various loans both in the UK and across the globe.

With overnight, one week and 1 to 12-month rates, the figures are calculated by a group of 20 contributing banks electronically forwarding their costs of borrowing to the Inter-Continental Exchange (ICE). However, the 3-month LIBOR is generally seen as the benchmark. The top and bottom quartiles are removed, and an average is taken of the rest.

In addition to mortgages that are explicitly linked to it, LIBOR has a direct impact on short-term variable rate mortgages – such as 2-year trackers and discounted trackers.

Is the LIBOR Legitimate?

The LIBOR was introduced into the money markets in the 1960s as a means of pegging average funding costs amongst a number of “reference” banking institutions. However, in the years following the 2007/08 financial crisis, its legitimacy was questioned when evidence emerged that the rate was increasingly “subject to manipulation”.

Banks were reportedly colluding to advantageously position their individual trades or provide an illusion of credit worthiness. Such institutions would also indiscriminately exploit loopholes within LIBOR itself, capitalising on what was subsequently deemed as a weak internal governance system. Such activity culminated in a number of high profile court cases and, to many people’s disdain, just one conviction.

Following an independent review and competitive tendering process, the Intercontinental Exchange (ICE) took over from the British Bankers Association (BBA) as official administrators of LIBOR in February 2014 – promising to deliver a tougher and more transparent governance framework.

Interest Rate SWAPs for Buy-to-Let Investors

Lenders and other financial institutions enter into SWAP-based contracts with each other to hedge against wholesale borrowing risks.

These contracts are often a solid indicator of overall conditions in fixed income markets and are used to gauge the pricing of corporate bonds, loans and mortgages.

In the mortgage sector specifically, the calculation can assume that a lender “borrows” funds from savers at a floating (variable) rate that are subsequently lent to mortgagors at a fixed rate. When interest rates remain low, there are no imminent risks for the mortgage lender (as savers must settle for lower rates in such an environment). However, things can become more problematic when interest rates rise, and savers look for more appealing rates. With fixed mortgage receivables, competitive pressures force the lender to offer better savings rates even though its margins will be negatively affected.

Meanwhile, another financial institution funds its operation on a fixed rate basis and earns income from variable (floating) rate lending. Facing the opposite conundrum, it would make sense to reduce the uncertainty resulting from variances in its own funding costs.

A SWAP contract agreement, in its most vanilla form, allows for both parties to align their liabilities and ensure consistent margins – regardless of which direction interest rates (typically LIBORs) move.

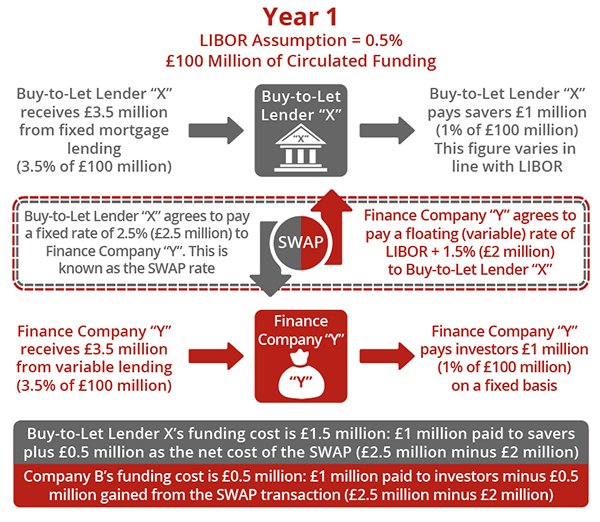

A hypothetical example of a SWAP in the buy-to-let sector

The figures in the example below have been broadly extracted from the Council of Mortgage Lenders’ blog.

Buy-to-Let Lender “X” finances its activities through borrowing from savers at variable rates based on LIBOR movements. It receives fixed income from its mortgage lending. The lender is concerned about the risk of a rising LIBOR, which would mean that it would need to pay more to savers without having the flexibility of increasing the amount of income it receives from mortgage borrowers.

Finance Company “Y” receives income from variable rate lending and has underlying fixed funding costs. It is looking to incorporate a floating aspect into its overall financing structure.

The two institutions enter into a SWAP contract.

Buy-to-Let Lender “X” forms an agreement with Finance Company “Y” on the basis of a 5-year swap contract on their underlying funds valued at £100 million. Buy-to-Let Lender “X” agrees to pay a 2.5% fixed amount on the £100 million (or £2.5 million) to Finance Company “Y” on an annual basis. Over the same period, Finance Company “Y” will pay a floating rate of 1.5% plus LIBOR to Buy-to-Let Lender “X” on the same amount of funding.

In year 1, illustrated below, the assumed LIBOR is at 0.5%:

Buy-to-Let Lender “X” has a funding cost of £1.5 million – constituting of £1 million paid to savers plus a £0.5 million “loss” payable to Finance Company “Y” (£2.5 million minus £2 million) as agreed in the SWAP contract. Finance Company “Y” therefore has a funding cost of £0.5 million made up of £1 million paid to its investors minus £0.5 million “gained” from the SWAP transaction.

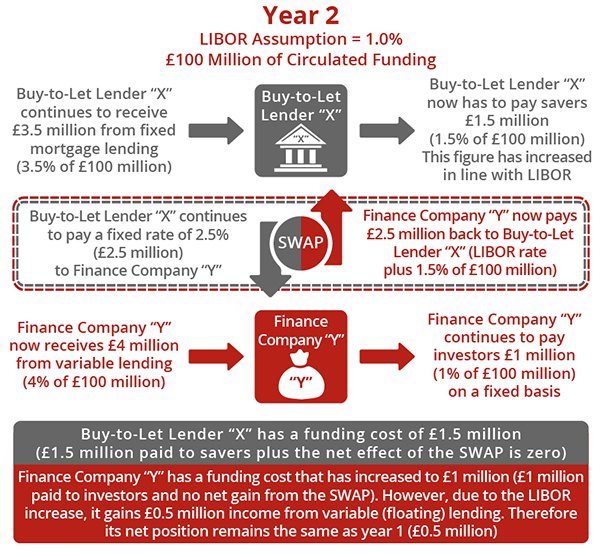

In year 2, LIBOR has increased to 1%:

As a result of the SWAP Contract, Buy-to-Let Lender “X” still has a funding cost of £1.5 million (the same as year 1). Even though the amount paid to savers has increased (to £1.5 million), the SWAP agreement dictates that it does not have to pay any extra funding to Finance Company “Y” (as was the case in year 1). Finance Company “Y” sees its funding cost remaining the same as year 1 – it still must pay the fixed rate of £1 million to investors and, although not “gaining” from the swap, it has earnt extra income from its variable lending. Its net position is still therefore at £0.5 million.

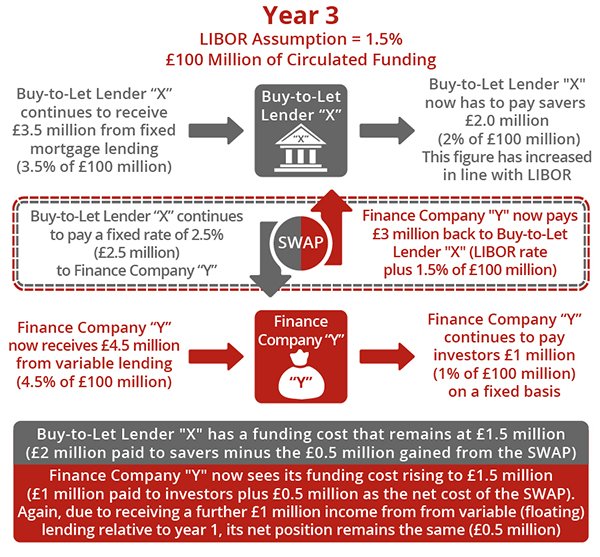

In year 3, the LIBOR has risen to 1.5%:

Again, Buy-to-Let Lender “X” has a funding cost that remains at £1.5 million (the same as years 1 and 2). This is because, even though the amount paid to savers has increased again to £2 million, it has now “gained” £0.5 million from Finance Company “Y” as a result of the SWAP. Finance Company “Y” must pay the fixed rate of £1 million to investors and, although losing £0.5 million from the SWAP, it has £1 million in extra income from its variable lending relative to its position to year 1. Its net position is still therefore £0.5 million.

These examples demonstrate that, regardless of how high the LIBOR rises, the net effects remain the same for both parties as a result of the pre-agreed SWAP contract.

Mortgage Lender Risk Averseness Towards Buy-to-Let (Micro)

There have been times in buy-to-let’s history where uninhibited mortgage lending overshadowed any notion of sustainable growth.

Although low deposit requirements and other loose underwriting policies may have made business sense at the time, the subsequent risks of loan book exposure are likely to materialise at some point. For instance, in areas that have not witnessed capital growth since the financial crisis, lender concerns about highly-geared landlords’ susceptibility to factors such as Section 24 of the Finance (No. 2) Act 2015 would certainly be warranted.

Whilst expecting such speculative trends to disappear forever would perhaps be unrealistic, some lessons have been learnt (albeit forcibly). For example, the Mortgage Market Reviews’ remit to drive more responsible lending eventually filtered into the buy-to-let sector by virtue of the Prudential Regulation Authority (PRA) stress-testing criteria. Introduced in January 2017, even though actual buy-to-let borrowing rates remain low, lenders must now ensure that any property must be comfortably stress-tested using a 5.5% payrate with an interest coverage ratio on the gross rent of 145%.

Furthermore, lenders must also take a holistic viewpoint on borrowers’ personal liabilities – factoring in Section 24 of the Finance (No. 2 Act) and other perceived risks. As a result, many brokers are expecting a mortgage and remortgaging “crunch”, principally due to the higher deposits needed to secure borrowing (see one of our Tweets on these extra requirements). It is also worth noting the other macro-prudential regulation (briefly explored below). This also highlights the need to have savings and the fact the once-popular ‘no money down’ strategy is practically impossible.

However, in spite of the inevitable slowdown in buy-to-let’s growth, these stricter underwriting requirements could create a more sustainable marketplace. Although there will be a smaller pool of buy-to-let properties to lend on, the probability of mass defaults is lower. We also believe there will be strong appetite for lenders to work with professional investors with long-term outlooks. Meanwhile, competition amongst key lenders should ensure that buy-to-let mortgage borrowers can access the best products.

Limited Company Buy-to-Let Mortgage Criteria

Even though the underwriting process for buy-to-let properties acquired using Limited companies (Special Purpose Vehicles) is not governed by the PRA, most lenders are likely to adopt similarly strict criteria moving forward.

Please see our previous post on applying for a limited company buy-to-let mortgage, within which explores how investors can build a “corporatised” portfolio.

Macro-Prudential Regulation

Having more of an over-arching influence over the buy-to-let lending market, a series of post-crisis financial regulations take direct aim at the banking industry’s previous attempts to “game the system” whilst instilling more resilience in the event of future economic downturns.

Basel III

This accord, referred to as the global financial “rulebook”, requires banks (and insurance companies) to have a number of specific internal regulations in place – namely:

- Risk-weighted capital held as reserves in addition to a mandatory “capital conservation buffer” and a discretionary “counter-cyclical buffer”;

- A non-risk-based leverage ratio set at over 3% – calculated by dividing the bank’s core capital by its average total consolidated debts (exposure);

- A Liquidity Coverage Ratio (requiring banks to hold a sufficient amount of highly liquid assets to cover its net cash outflows over 30 days);

- A Net Stable Funding Ratio (measures the proportion of secured funding that can weather a period of extended stress without eroding a bank’s liquidity position).

At the same time, it is expected that the removal of requirements that smaller lenders must have the same amount of capital as larger institutions will level the playing field somewhat.

IFRS-9 (International Financial Reporting Standard No. 9)

Issued by the International Accounting Standards Board (IASB), the IFRS 9 governs mortgage lenders internal accounting treatments. The standards essentially create an obligation for lenders to have a sufficient level of reserves in place to mitigate the effects of anticipated bad debt – irrespective of whether issues such as arrears have been experienced or not.

The amount of required reserves is determined by the amount of potential losses throughout the lifetime of the mortgage (not just the initial term). Mortgage lenders must also disclose key figures and ensure that their ongoing activities are appropriately adjusted for risk. Such information will be available in the public domain.

Markets in Financial Instruments Directive II (MiFID II)

Seven years in development, the introduction of some 1.5 million paragraphs of rules aimed at making European markets safer, more transparent and efficient will affect a range of verticals across the banking industry.

The Financial Conduct Authority (FCA) has confirmed that MiFID II will apply in the UK until it fully leaves the European Union. After that point, the UK will need to make its own decision as to whether it wishes to follow the rules.

Conclusions – Securing Your Buy-to-Let Mortgage

For the foreseeable future, with buy-to-let lenders taking a more cautious approach to the design and structure of their mortgages, investors are likely to find that more conservative approaches to due diligence will prevail.

We strongly recommend taking the time to understand the true implications of acquiring and holding buy-to-let property, and use the same frames of reference as lenders. The stress-testing section of our buy-to-let financial calculator, for example, allows users to adjust a wide range of factors including the interest only mortgage rate, deposit input, market value, voids, new tenancy, recurring and contingency costs.