Coinciding with the release of the delayed “broken market” White Paper, the annual British Property Federation (BPF) Residential Conference sought to address a number of pertinent housing-related topics of the day. Principally chaired by Bill Hughes, Head of Real Assets at Legal & General Investment Management, the various presentations and panel discussions delved into a number of key issues ranging from planning to London´s affordable housing crisis and the supporting role of government at local and national levels. The latter part of the day focused heavily on build to rent (outlined in a separate blog post), a tenure that benefitted from further traction by means of consultation on changing the National Planning Policy Framework (NPPF) (recommending that local authorities plan proactively for these schemes and allow discounted market rent to complement other forms of affordable housing provision). On this latter subject, readers may be interest in reading The Property Investor Blog´s interview with BPF policy director and lobbyist Ian Fletcher.

“Key Planning Issues”

Joe Sarling of Lichfields (voted planning consultancy of the year by the Royal Town Planning Institute) gave the first keynote of the day entitled “Finding Scale in a World of Complexity” in which the content of three relevant research pieces was outlined:

“Early Adopters and the Late Majority” – A Review of Local Plan Progress and Housing Requirements – published in April 2016 (and therefore subject to some statistical revision), this report sought to analyse the progress of implementing Local Plans within the National Planning Policy Framework (NPPF). Some of the key takeaways are summarised below:

- Of the 139 Local Plans examined or submitted for examination, 86 were deemed as being “sound”;

- Of the Local Plans described as “sound”, 48% have had to increase their housing requirement in order to address objectively assessed housing needs (OAN);

- 19% of planned supply exceeds household projections in aggregate within up-to-date Local Plans;

- One-third of Local Plans are up to date post-NPPF and it is deemed that 21 Local Planning Authorities are most “at risk” of Government intervention;

- 1 in 15 Local Plans examined have been found to fail the Duty to Cooperate (a legal duty under the Localism Act 2011 on local planning authorities, county councils and public bodies to engage constructively, actively and on an ongoing basis to maximise the effectiveness of Local Plan preparation in the context of strategic cross boundary matters);

- The Local Plans Expert Group (LPEG), established in September 2015, was tasked with simplifying the system under the “aim of slashing the amount of time it takes for local authorities to get them in place”;

- Plan-making has been markedly slower in authorities with significant areas of Green Belt. Current policy, it is argued, has created a disincentive to prepare Local Plans for those areas seeking to protect their Green Belt. With the government affirming that Green Belt land as “sacrosanct”, any associated policy is unlikely to change for the foreseeable future. Local Planning Authorities should have to continue to have to define Green Belt boundaries within Local Plans, ensuring consistency with the local plan strategy to meet identified requirements for sustainable development. The Local Plans Expert Group (LPEG) has advised that the Green Belt is a “planning mechanism rather than an environmental designation”;

- As confirmed in the 2017 White Paper, where local planning authorities have not produced / updated a Local Plan, government will be able to intervene to arrange for a plan to be written;

- LPEG recommend all Local Plans should be submitted alongside evidence that provides a proportionate Assessment of Environmental Capacity;

- Where Local Planning Authorities (LPAs) seek to justify a housing requirement below housing need for their own area by reference to capacity constraints, they will need clear and coherent evidence demonstrating that an area could simply not carry the level of development necessary to meet housing needs (evidenced by environmental impacts, landscape sensitivity, habitats regulation and other constraining assessments);

- The LPEG recommends that the duty can be given “bite” by requiring LPAs to enter into a memorandum of understanding which would ensure that housing needs across or between Housing Market Assessments (HMAs) are fully addressed;

- The LPEG sets out recommendations on how Local Plans and LPAs can ensure more effective land supply, including allocating reserve sites as a 20% buffer to the housing trajectory;

- There will be a need for land supply to get to grips with the patchwork of mechanisms for allocating sites for development, with most LPAs expected to have a mix of strategic allocations, sites on brownfield registers (benefitting from Permission in Principle), Neighbourhood Plans, Site Allocations Plans and Housing Implementation Strategies;

- With Local Authority planning budgets halved in real terms over the past six years, the LPEG recommends that more concise Local Plans are in place – supported by a more succinct and focused evidence base.

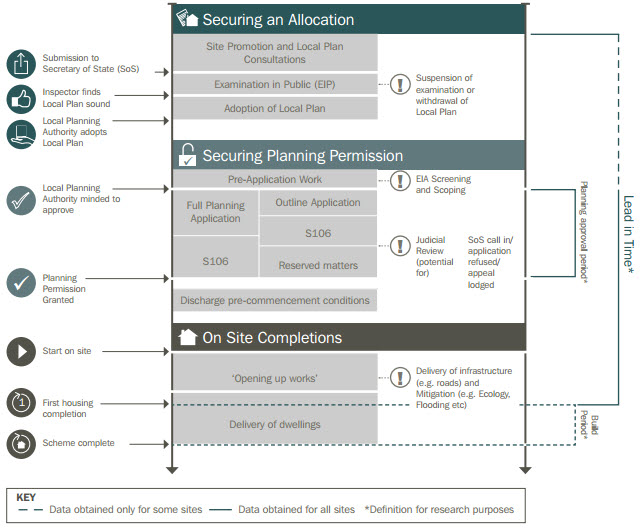

“Start to Finish” – How Quickly do Large-Scale Housing Sites Deliver?” – Published in November 2016, the report highlighted the role of large-scale housing developments in meeting the government´s target of 300,000 units per year. Some of the noteworthy points of the report and presentation are outlined below:

- Of the 70 large (strategic) assessed sites outside of London, the average lead time prior to the submission of the first planning application was 3.9 years. Schemes of over 2,000 units took an average of 6.1 years to receive planning approval with the average of all large sites being 5 years. The average annual build rate for schemes of over 2,000 units was 161. 50% more homes per annum are delivered on average on large greenfield sites than large brownfield sites;

- Should the government genuinely desire more homes to be built, it will be a simple case of releasing more land and granting more planning permissions;

- Larger site planning applications take longer due to the complex planning issues related to both the principle of development and the detail of implementation;

- Where matters are substantially addressed prior to the application being submitted, planning applications are determined more quickly than average;

- The timeline for the delivery of a strategic housing site is outlined in the diagram below:

- Planned housing trajectories should be realistic, accounting and responding to lapse rates, lead-in times and sensible build rates. As each site has its own variations in terms of lead-in time and build rates, a sensible approach to evidence and justification is required;

- Local authority spatial strategies should appreciate that developing is a complex and risky business;

- Absorption rates for all developments are directly correlated to: the ebbs and flows of the local housing market (weaker areas may not be able to sustain high build-out rates); the number of sales outlets; competition and tenure (for example, whether market homes for sale are supplemented by homes for rent and affordable stock);

- Evidence suggests that the higher the affordable housing proportion, the higher the output per year. This principle is also likely to apply to other sectors that complement market housing for sale, such as build to rent and self-build (providing there is demand).

“Stock and Flow: Planning Permission and Housing Output” – this report (released in January 2017) primarily explored housebuilder and land promoter business models; the risks associated of bringing new homes forward through the planning system and whether accusations land banking are consistent with the development industry´s own commercial drivers. The report also addresses the quantity of planning permissions required to secure the housing supply necessary to meet long term needs.

- 261,644 homes were granted planning permissions in 2015;

- Of the 189,650 net completions, 163,940 were new build;

- Lichfield believes that there is insufficient understanding of the relationship between planning permissions and completions as well as of industry stakeholder commercial objectives;

- Appreciating the riskiness of all stages of the housebuilding process, land banking is considered to be “irrational behaviour” for developers. Notions of “gaming” to deliberately choke off supply or slow down development in anticipation of land value appreciation are empirically unsupportable. House builders, largely operating as “price takers” rather than “price setters”, are structured to build and sell as quickly as possible due to the myriad of financial “holding” and other practical costs. Despite the media attention surrounding the issue, land banking in the housebuilding industry has also been examined and rejected by the Barker Review (2004), the Callcutt Review (2007) and the Office for Fair Trading (2008);

- Land promoters / developers are well aware that chances of getting planning permission on sites (with dischargeable pre-commencement conditions) are certainly not guaranteed, even if sites are allocated in Local Plans. Costs, timescales, technical complexities and market cyclicality concerns collectively exacerbate risks and highlight the need for projects to be executed within in a timely manner;

- In relation to site build-out rates it was observed that, due to scaling advantages, larger sites deliver more homes than smaller sites;

- House builders rarely have the option of building out sites more quickly than the natural absorption rate for their product on that site. If a company sought to increase the supply of homes on a site faster than the rate consistent with market values, it would either not be able to secure land in the face of competition from other house builders; or have sales values inconsistent with its agreed land price, thus eroding its site margins;

- The Local Government Association (LGA) estimated a stock of 475,000 housing units on unimplemented sites, a relatively small figure considering the number of homes built each year, the length of time to build out, the variety and number of sites in the pipeline required to signal to investors that developers are worth investing in. Importantly, the data is collected on sites at planning and contract stages, not monitored actual completions – so a scheme that is 99% completed would show up as “unimplemented”;

- Civitas analysis, that compared the number of units with planning permission and housing starts on site, did not cater for recognised lapse rates (see below) as well as time periods between a new permission being granted and when a site can practically be started (which varies according to site location, planning policy, planning obligations, market cycles, investment appetite and political priorities);

- Planning permissions can lapse for a number of reasons including: landowner reluctance to sell at a price that provides the land promoter / developer a sufficient margin; the development is not considered to be financially worthwhile; financing constraints; changing priorities; re-planning proposals and pre-commencement conditions take longer than anticipated to discharge. The national picture is skewed by the very high lapse rates which occur in London (50% according to GLA 2014 research based on sites of 20 dwellings or more);

- While entire sites are granted permission in one year, actual development will not occur in the same year (given lead-in times) and may happen over a number of years, depending on the size of the scheme;

- For any 100,000 dwellings granted permission and which do not lapse, just 50,000 could be expected to be completed in year one of the development, 25,000 in year two, 14,000 in year three and so on. This reflects that over half of all units with permission are on sites that are expected to build out over more than one year. Thus a year’s worth of permissions would inevitably not translate into the same number of housing completions the following year, but would result in a staggered output as the larger sites are built out;

- Requiring an analysis of flow rather than stock levels, Lichfield estimates the number of live permissions required to meet government-led housing target numbers by adding the number of units with new permission granted in that year plus any unbuilt permissions from previous years;

- From pages 15-17 of the report Lichfield run through two scenarios: an average of 245,000 net additional dwellings per annum over a 10-year period and an average 300,000 net additional dwellings per annum from 2016 to 2025. Applying a number of lapse rate, demolitions and permitted development completion assumptions, it is concluded that there is good reason to be confident – all things being equal (and assuming the construction sector can deliver) – of achieving the government’s one million homes target during this Parliament. Interestingly, when the audience was asked who believed that such a target was possible – very few hands were raised.

“When (London) Brownfield Isn´t Enough”

Barney Stringer, director at Quod summarised the main findings of a report compiled in collaboration with Shelter that explored strategic options directed towards London´s growth and confronting the affordability crisis defined by increasing numbers struggling with rent, families in cramped conditions and at risk of homelessness. Produced in early 2016, most of the findings are relevant today – serving to shape the direction of London Plan (see Jules Pipe, London´s deputy mayor for planning presentation summary below). The paper explores some of the main options which, whilst possessing their own advantages and limitations, could potentially be deployed in a mutually dependent manner:

- Brownfield Redevelopment – one of the immediately thought of solutions for London housing. It is noted, however, that bringing such sites into use can be slow, difficult and expensive. The “easiest” sites in in the Capital have already been developed and there are other barriers including bringing together sites in multiple ownership, relocating existing users, decontamination, planning permission constraints and practical issues related to executing the development itself. The faster release of Strategic Industrial Land is suggested (avoiding the crowding out of essential manufacturing / distribution through greenbelt substitution) – as is removing the barriers that make such sites difficult to develop and encouraging public investment in local infrastructure, particularly transport. Mixed-use projects can also spur job creation and ease the pressure on housing;

- Taller Buildings – such proposals may be blocked for their effect on the character and setting of certain parts of London. The Capital´s five airports and aerodromes also have essential height restrictions that extend many miles around. Rules on density can effectively limit heights and not everyone will want to live in tower blocks. The challenge will be to create well-designed buildings that are not akin to 1960s-style towers (which, it is argued, were sometimes a less efficient use of land than more traditional terraced streets). A balance will have to be struck between protecting the current skyline and allowing a change in heights;

- Green Belt Growth – the full London Green Belt, extending into the wider South East of England is huge (covering four times as much land as the built-up area of London). With only one fifth having environmental status or accessible to the public as green space, the Green Belt is intended to limit the outward growth of London into the countryside and enveloping surrounding towns. The difficulty will be moving beyond the widespread public support for Green belt protection in line with the sustainable development of new homes with the right infrastructure;

- Garden Cities or New Towns – the displacement of growth into new settlements outside London can potentially reduce the pressure on tricky land options, such as brownfield regeneration mentioned above. However, an active willingness would be required on local governments and authorities outside of London and, with the slow planning and build out rates, the capacity to provide a large number of new homes quickly is limited;

- Estate Redevelopment or Infill – the aim would be to improve the density of some housing estates in a coordinated and systematic manner. Good estate renewal, it is noted, could take decades to accomplish effectively and there would be a range of practical issues including the relocation of existing tenants and ensuring minimum disruption. New homes will need to pay for the re-provision of old homes and costs and delays are added by the need for compulsory purchase powers and to re-purchase leaseholds sold under “right-to-buy”;

- Increasing Density in Suburbs – with 20% of London’s population occupying 40% of London’s residential land, if the number of homes in low density suburbs could be incrementally increased by 10%, 75,000 homes could be delivered. However, research has suggested that London suburbia is less supportive of such expansion and fragmented private land ownership means comprehensive change is not easy achievable other than in a gradual and piecemeal way. Subdivision (of houses into flats, for example) certainly has a role to play, but there are limits as to how much this can achieve. It is also noted that dispersed growth can make it difficult to plan investment in social infrastructure such as schools, healthcare etc.;

- New Transport for New Homes – with future rail projects increasingly being planned on the basis of how much housing can be delivered, a maintained pipeline of future investment should be in place. Projects mentioned, in addition to Crossrail 1 (due to open in 2018), include The Northern Line extension to Battersea (due to open by 2020); the Barking Riverside extension (proposed to open in 2021); High Speed 2 and Old Oak Common (first phase due in 2026); Crossrail 2 (could open around 2030) and the Bakerloo line extension (proposed for around 2030). Bold decisions and careful planning will be required on the routing of these schemes;

- High Density Town Centres – smaller suburban town centres may struggle to survive changing shopping habits which may well require them to find a different future. The Greater London Authority (GLA) has identified 220 town centres with potential for wider housing capacity (albeit with suitability and capacity varying hugely) and has estimated the potential deliver of over 15,000 new homes a year. However, progress has been slow due to a reluctance to accept a shift away from employment uses. There are also questions regarding policies intended to promote family housing that may not work well when applied rigidly to locations more suitable for younger adults and older people as well as reticence to accept taller residential buildings in the heart of a lower-rise suburban communities.

These write ups and ongoing research are brought in line with the ongoing land finding and promotion work of PS Development Services.