Build to Rent (BTR) dominated much of the afternoon´s discussions at the annual British Property Federation (BPR) Residential Conference, starting with a look at a recent report published by Savills in conjunction with the BPR, Barclays and the London School of Economics (LSE) entitled “Build to Rent – Unlocking the Potential of an Emerging Property Sector”. A presentation by Jacqui Daly, director or residential investment research and consultancy at Savills as well as some the core findings of the report are summarised below:

- Whilst 98% of the £1 trillion PRS sector is tied up in the hands of small landlords, the pipeline of bespoke build to rent (BTR) stock is increasing;

- The perceived beneficial impacts of purpose-built PRS developments on overall housing supply include: accelerated delivery (more noticeably on larger urban sites); faster market absorption rates that benefits regeneration and placemaking; viability in markets where build-to-sell is marginal; improved service to tenants and job creation;

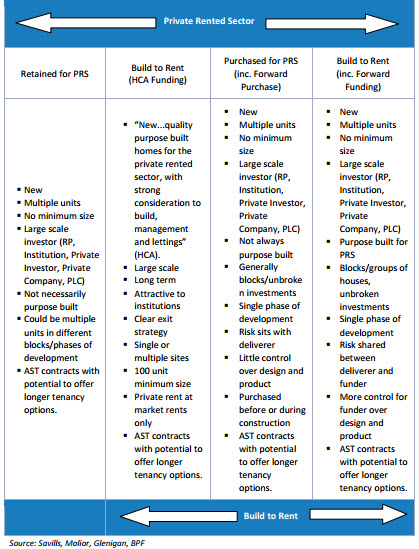

- The table below outlines the delivery approaches that have been used – the common factor across the different types of stock is that the rental supply is all new multiple units, in single ownership and professionally managed:

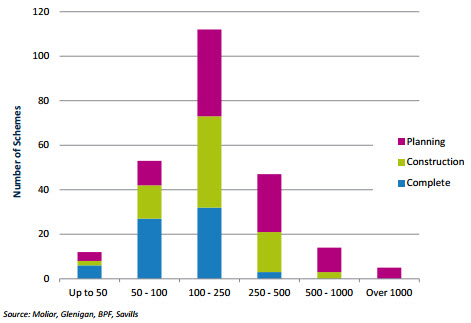

- The current total number of schemes and units by scheme size across England and Wales is demonstrated in the graph below:

- According to the research, many schemes comprised of units originally planned for market sale which were then purchased for the rented sector. However, looking ahead, there is a much higher number of purpose-built units planned for development;

- The scale of projects is increasing which is creating funding challenges. Stakeholder concerns include the relatively speculative nature of the overall business model; lower capital values (compared to build to sell projects); vulnerable gross-to-net leakage; higher sinking fund requirements as well as a lack of transparency, market references, valuation and other empirical evidence;

- Conversely, operating and management expenditure are much easier to quantify. It is argued that purpose designed, specified and built BTR assets can provide more certainty and enhance long term value for investors;

- The research suggests that the most effective policies in overcoming market failures, delivering new additional homes and realising the benefits of build to rent include: clarifying the role of Discounted Market Rent (DMR) in meeting affordable housing requirements (to limit the displacement risk in major cities such as London); changing planning regulations and standards specific to the sector; continuing public sector development loans (extending the Homebuilders fund to the PRS, for example); extension by time and scope of the PRS Debt Guarantee scheme; covenants to guarantee longer term tenancies; s.106 clawback mechanisms; planning preference for larger sites;

- Whilst there were no provisions in the Housing White Paper, calls will continue to be made to exempt large-scale investors from the 3% stamp duty surcharge and zero-rate VAT on repairs / management costs.

“Learning from Other Assets”

Chaired by Ian Marcus, Senior Consultant at Eastdil Secured, two presentations by Ana Nekhamkin, Managing Director at Inhabit and Paul Hadaway, Chief Executive, Empiric Student Property highlighted the importance of creating service-led outcomes when planning for, executing and managing build to rent developments.

Inhabit is a privately-owned, UK based BTR platform with plans to build 3,500 units across the country. Ana Nekhamkin´s presentation focused on her own experiences in the hotel industry and other asset-backed operating businesses (referring to projects such as the KPMG Offices Mayfair, Second Home London, Student Hotel Eindhoven, Zoku Amsterdam and Ralph´s Coffee & Bar London).

- Highlighting the importance of branding, design, pre-opening, operations, financing and structure as the prominent components of a successful scheme Nekhamkin referenced the Four Seasons, Generator, swissôtel and Premier Inn. Creating brand loyalty, and thereby make the offer less “commoditised” will be most likely to boost turnover and lower overall marketing spend. A good brand will ultimately be based on a solid understanding of the target demographic(s) and will manifest itself through a consistent operational structure that is emotionally connected to customers;

- With BTR schemes more likely to present volatile cash flows, incentivising longer tenancies will be a priority for management teams;

- The building blocks of any successful BTR scheme will be made of effective service delivery, IT provision, revenue management, sales & marketing, HR / training, events / PR, maintenance / repairs and ancillary revenues;

- A well-designed scheme in a good location with active communal spaces combined with whole life cycle considerations can be a significant driver of rental premiums on BTR schemes and, according to Nekhamkin, does not necessarily need to be expensive;

- How a BTR chooses to operate will also be important – services from branding to daily operations may be outsourced, kept-in house or based upon some form of hybrid model.

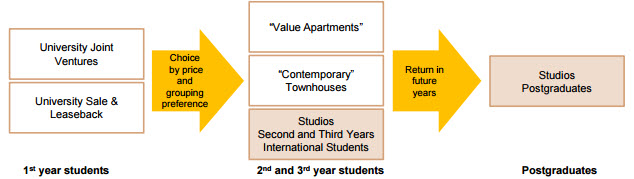

Paul Hadaway of Empiric provided some interesting insights into the high-spec student development model. The company has an IPO target of 10,000 beds in 5 years (2014) with a target list of 36 cities selected by popularity of universities and is engaging in joint ventures to achieve its objectives in line with the solid expectation of tertiary education growth in the coming years:

- Notwithstanding the more established nature of the business model, as an asset-backed, pseudo-commercial business proposition, build to let and student accommodation share several of the same characteristics in terms of return dynamics (op co / prop co distinctions, income based valuations, service-led operational structures);

- Supply / demand fundamentals persist across the full spectrum of the fragmented UK student accommodation sector. With a large dominance of poor-quality student “digs”, there is scope to deliver better homes for students throughout the full higher education life cycle:

- Reputation and quality standards are fundamental to ensure market longevity. The provision of gyms, cinemas and shared work rooms are some of the supplementary services that need to be built into student schemes;

- The industry risks mentioned included questions regarding whether university represents value for money, protectionism / visa issues (controlled immigration) and the falling value of Sterling. In terms of opportunity, there is a stable long-term income from high yielding property, enhanced NOI from branded portfolios which are targeted at defined sub-sets of customers.

Tête-à-Tête – Cost Engineering

A discussion between Mark Farmer, chief executive at Cast Consultancy (author of the industry-recognised 2016 “Modernise of Die” Farmer Review), Lesley Roberts, executive development director at Allsop Letting & Management and Russell Pedley, co-founder and director of Assael Architecture largely focused on some of the more practical issues involved with build to rent management and continued the theme of prioritising good service provision at minimum cost.

- BTR schemes will inevitably be dual-pronged, focused on capex optimisation and revenue generation. Residual valuation methodology is therefore different to build to sell schemes and it was argued that, with very little “critical mass”, the ability to accurately model the sector still has some way to go. The challenge, as echoed in the preceding discussions, was that there is very little track record and understanding as to how schemes operate over the mid-long term;

- From a Net Operating Income (NOI) perspective, design and build decisions should be focused on cost efficiency in conjunction with value creation and quality;

- It was argued, particularly by architect Russell Pedley, that key ongoing issues such as the turnover (churn) of tenants, changing lifestyle and demographic patterns are not being considered by schemes being bought forward. A 5 year hold strategy will be very different to a 25 year hold, for example;

- The right design is also fundamental for everyday management of the building in terms of staff wellness and back office functions. Brand and development ethos will be shaped by the personality and cohesiveness of management teams, coupled with the latest leasing and tenant interaction technologies. Attracting the right kind of staff will be essential. Particularly with larger projects, Pedley also referred to the risk of BTR developments becoming “soulless” and, whilst calls of smaller space standards may make projects look attractive on paper, developers should ensure the appeal factor is regularly maintained and understand that one size does not fit all;

- As time moves on and the sector matures, data can be used to navigate around the above issues – particularly with regards to behavioural patterns and other intangible factors that can, with varying degrees of accuracy, revert back to the cost-engineering processes. There will indeed be different PRS sub-sectors and varying scheme configurations / amenity provision based on specific target markets;

- As a thought leader on the topic of modern methods of construction (MMC), Mark Farmer raised the question of modular and prefabricated methodologies being introduced into the sector, as has increasingly been the case in student schemes. Citing the example of pod and other modular approaches, whilst the potential efficiencies to be gained should certainly not be understated, many of new building methodologies are at the embryonic stages of development. Building Information Modelling (BIM) was also mentioned as a means of gaining more accurate costings data.

“The Different Approaches to Build to Rent”

Chaired by Sharon Quinland, managing director, Real Estate London at Barclays, one of the last discussions of the day bought together a group of active Build to Let developers – namely Mark Allnutt, managing director at UK Multifamily Greystar; Johnny Caddick, managing director at Moda Living; Lesley Chan Davison, portfolio and corporate finance executive at Delancey and David Cowans, group chief executive at Places for People. Some of the challenges and opportunities of the sector were discussed:

- Build to rent is at a similar stage where the student market was 10 years ago, building momentum and finding its own path. Governments are unlikely to make things happen for the sector but should be willing and able to create appropriate frameworks to ensure sustainable growth;

- Within London and other larger conurbations, there will be an increasing need to cater to all incomes without compromising on quality standards. Labelling units as “affordable” is not always helpful – for example Lesley Chan stated how there are 8 tiers of income requirements in the up-and-coming Delancey schemes;

- The challenge in catering to different income groups will be ensuring that projects commercially viable. The consensus was that scale would be key and Mark Allnutt of Greystar also mentioned a West London project in partnership with the local council. There are also potential overlaps with shared ownership and rent-to-own models;

- Other indicators of good scheme outcomes will be location, site purchasing at the right time in the property cycle, long-term retention (lower churn) and ensuring that there is income certainty / minimal rental elasticity;

- Competition for sites with both build to sell and build to rent developers moving forward is expected to increase. It was also noted that with BTR schemes outside of London, there is a lot of pressure and challenging in establishing capital values;

- David Cowans of Places for Peoples explained how building infrastructure on hypothecated sites prior to housing enables projects to be eased into the community structure, overcomes a number of NIMBY-led issues. This option is, however, only available for larger and well-capitalised developers and those that can afford to be flexible with regards to delayed build-out;

- With regards to financing, the institutional investment momentum looks set to continue and the Middle East is also finding UK BTR interesting – particularly with the discount on the pound to the dollar. RPI-indexed income is not the only component of the business model and BTR looks set to uniquely benefit from design-build-operate blended long-term yields / returns.

These write ups and ongoing research are brought in line with the ongoing land finding and promotion work of PS Development Services.