Part 2 – Focus on Post-Brexit Planning and Housing Supply

The second part of the late-2016 Planning Resource event (see part 1 here) addressed a number of topics ranging from the “Brexit effect” on migration and household composition, infrastructure development and the future of planning through to innovative Housing Association-led development models and how London can overcome its affordable housing delivery challenges. The afternoon was chaired by Duncan Sutherland, regeneration director at Sigma Capital Group Plc – a company at the forefront of the Private Rented Sector (PRS), working with local government to deploy an innovative £1 billion Sharia compliant fund to build 10,000 family houses.

Starting with a presentation entitled “Calculating housing need in a post-Brexit period: What Brexit means for plan-making”, James Donagh, Director at Barton Willmore explored how future migration could affect the pace of development growth.

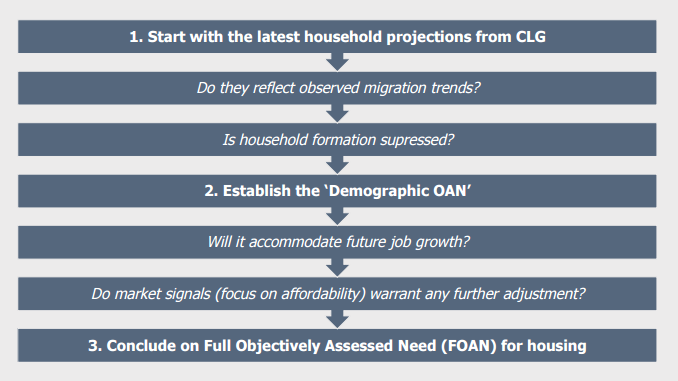

Donagh firstly referred to the principle of Full Objectively Assessed Need (FOAN) under paragraph 47 of the National Planning Policy Framework (NPPF) which states that: “to boost significantly the supply of housing, local planning authorities should … use their evidence base to ensure that their Local Plan meets the full, objectively assessed needs for market and affordable housing in the housing market area.” The Planning Policy Guidance (PPG) “Housing and Economic Development Needs Assessment” breaks down the methodology for assessing FOAN for housing:

Secondly, paragraph 159 of the NPPF states that Local Planning Authorities (LPAs) are required to have “a clear understanding of housing need in their area” and prepare a Strategic Housing Market Assessment that:

- meets household and population projections, taking into account migration and demographic change;

- addresses the needs for all types of housing; and

- caters to housing demand and the scale of housing supply necessary to meet demand.

Using the Office of National Statistics (ONS) most recent population projections, net migration levels stood at 335,000 to the year ending June 2016 with an estimated 10-year trend of 250,000 per annum. How migration and population growth will effect housing demand is still contingent on the post-Brexit political and economic climate. Donagh argued that net migration levels are likely to be lower if “Brexit actually means Brexit” and the UK becomes de facto separated from the institution of Europe – i.e. rejecting all EU regulations and replacing the EU Court of Justice jurisdiction with UK Courts. Conversely, should the UK be able to forge trade links with the EEA Single Market, incorporating some vestige of free movement, net migration figures could well be higher. However, certain sections of the public could claim that the latter course of action is too “soft” and contrary to the referendum result. The alternative proposition of falling back on WTO governed agreements could be a disruptive and costly way to move forward. Donagh also reminded us of the strong political desire to reduce net migration to the tens of thousands since 2010 and the current Minister of State for Immigration – Robert Goodwill – sees Brexit as an opportunity to raise control over borders by means of employer driven work permits and an Australian style points system (where the government effectively decides the relative “value” of different types of skills). However, as explored in the morning discussion, the ease of implementing such policy making will be another question. Both the US and Canadian points systems, Donagh commented, have witnessed undocumented and unofficial migrant flows.

Appreciating the relative strength and attractiveness of the UK economy as a major pull factor, Donagh concluded by given a “best guess” planning assumption of between 185,000 and 250,000 annual net migrants. However, questions are being raised with regards to household projections and how the statistics apply in real terms. He also caveated that these figures would require ongoing sensitivity testing on the basis of domestic population growth, the ageing population, suppressed household formation levels, housing over-supply considerations (for example in certain regions of the North and Midlands) and the potential effects of other adverse market signals.

The following presentation by Janice Morphet, Visting Professor at the UCL Bartlett School of Planning started by outlining that certain policy and legislation are likely to remain the same regardless of a hard or soft Brexit deal, including environmental and climate change (agreed through UN treaties); competition and procurement rules (agreed through the World Trade Organisation); and rules governing city regions and functional economic areas (agreed through the OECD). However transport, comprehensive networks, sustainable urban mobility plans and ports as well as a range of European Structural and Investment Fund (ESIF) and Local Enterprise Partnerships (LEP) / Combined Authority funded projects could all come under some form of threat. For example, the Professor argued that progress on the Trans-European Networks (through schemes such as HS2, the northern rail hub and the A14 trunk road improvements) has helped the UK government meet its treaty commitments and provided a “legal basis” to ensure priority for domestic and European funding. At the point when these treaties are annulled and have “no anchor”, a “litigious objector could ask what these projects rest on”, Professor Morphet commented. However, projects that are already underway or close to being started, such as the High Speed 2, will probably not be undermined.

According to the Professor, the UK may also be sacrificing its role as part of the European expanded infrastructure investment programme and post-2021 European Spatial Development Perspective (ESDP) as well as lose access to European Investment Bank – unless all 27 states agree on loan terms (approximately 50 billion euros was lent to the UK for housing in the last 5 years). Other cited concerns for planning and the housing sectors include the financial uncertainty risk to property investment; higher costs / less access to capital finance; the loss of the role of London; less labour sources leading to wage inflation; less taxation income to fund health and pensions and other pressures on government funding. In the event of a slowdown, the Professor added, planners can help maintain economic activity by going back to the intentions of the 1974 Act – i.e. include delivery as part of the planning process by means of Compulsory Purchase Orders (CPOs), site assembly, regeneration areas, zoning. Planners can also use the powers of the 2011 Localism Act s. 1-7 and new International Financial Reporting Standards (IFRS).

Moving on to discuss whether Brexit will impact on the government´s intent to scale up affordable housing delivery, the Professor outlined the importance of making public sector operators more responsible for capital budgets. Local governments can effectively become patient investors and build up their asset bases and income streams which, in turn, can be redirected to support social well-being and regeneration investment. Several local authorities are indeed beginning to operate more like corporate entities, competing or joint venturing with the private sector and moving more towards self-financed project outcomes – examples of which can be seen in Luton (Cheyne Capital’s £850 million investment in social housing); as a part of Manchester´s noteworthy growth plans the emergence of Local Authority Pension Funds across the country. Here, there will be a need to develop integrated master-planning strategies and collaborative mindsets that promote trust and minimise uncompensatable risks.

Mention was also made of the role of the New Homes Bonus (NHB) aimed at encouraging local authorities to grant planning permissions for the building of new houses in return for additional revenue. Under the scheme, the Government matches the Council Tax raised on each new home built. In 2017-18, NHB payments will be made for five, rather than six years. This payment period will be reduced again to four years from 2018-19 (note that Local Authorities are not obliged to use the Bonus funding for housing development).

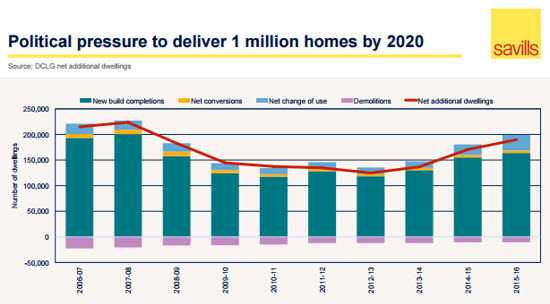

The next presentation by Susan Emmett, Director at Savills Residential Research entitled “How are housebuilders reacting to Brexit vote?”, started by summarising some of the potential economic ramifications of the summer 2016 decision, namely the impact of falling Sterling on inflation and possible rises in the Bank Base Rate (BBR) that could create eventual constraints on debt sourcing. Other highlighted concerns included stagnating wage growth, investment aversion, tighter lending criteria and tax changes in the buy to let sector. Overviewing housing market growth post-crisis using the Nationwide House Price Index, Emmett indicated two spikes during the course of 2009 (which was followed by a period of stagnation) then another uplift in 2013-14, slowing again since the introduction of the Mortgage Market Review (MMR).

There remains concerted pressure on developers to build homes, the pace of which is still below pre-crisis levels as demonstrated in the graph below (sourced via the DCLG):

Recent Housebuilding Federation (HBF) data has nonetheless indicated that site visitors and net reservations for new builds bounced back after a summer (2016) dip and the industry is currently building more houses than at any point in the last decade (163,940 new build completions in 2015/16). It is hoped that this pace of growth will continue in the coming years, irrespective of the widely expected turbulence resulting from the Brexit negotiations. However, the Savills latest Development Land Index has demonstrated how the market is very fragmented and developers are approaching new schemes with more caution. Other cited obstacles include planning delays, labour availability / costs, rising costs of non-domestically sourced material, land prices and land availability.

With the Autumn Statement´s tone of moving away from an exclusively homeownership agenda (a £1.4 billion grant fund for 40,000 affordable rented homes before 2021 is one example of this change in direction), Emmett referred to Savills recent report entitled “Releasing untapped potential for more housing”. Based on the analysis of 175 of the largest Housing Associations, in an effort to move away from purely market-driven development, Savills estimates that the sector could bring forward an additional 44,000 new homes per year by 2029 by means of asset-backed borrowing, improving efficiencies and using balance sheets more innovatively. Appreciating that increasing the delivery rate is a “long game” (as developers become more accustomed to operating with greater risk and market exposure), the hypothesis is explained diagrammatically on page 3 of the report. Housing delivery would be spread over four tenures: (i) market sale, (ii) shared ownership, (iii) market rent and (iv) affordable rent. Borrowing for build costs and land would total £7.4 billion (with shared ownership and affordable units costing less to produce). With £3.9 billion of proceeds generated from market and first tranche sales combined with annual rents of £0.2 billion (providing a gearing capacity of £3.7 billion), assuming a cash interest cover ratio of 1.5 at 3% cost of debt backed against a £4.7 billion asset base, the result would produce a recycled working capital level of £7.7 billion.

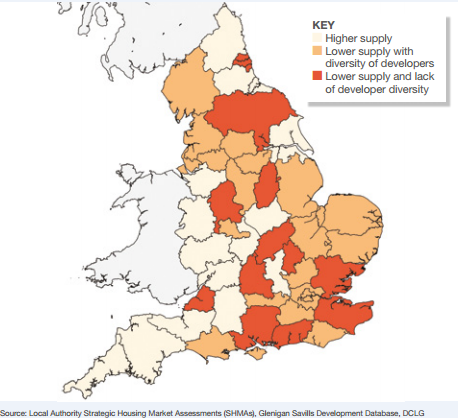

The dark red parts of the map below (extracted from the report) highlight the counties that witness the lowest levels of housing supply and the least diversity of developer types. It is claimed that Housing Associations are “well placed to be part of the solution” to boosting the range of tenures supplied to these local markets.

It is deemed that the projects would be largely undertaken by large scale voluntary transfer (LSVT) associations who have experience of managing extensive rented housing portfolios. Homes for sale would be delivered during a bullish market and rental units in leaner times. The structure of Housing Associations allows for the continuous delivery of schemes regardless of market peaks and troughs or periods of tighter development funding. Some flexibility will be required from Local Planning Authorities on delivery timings who should also be encouraged to take more of a leadership role in land assembly and contribution of surplus assets.

This hypothesis assumes current market conditions for building average new homes in an average market in the south of England outside London and it should be observed that higher inflation conditions / interest rates would require different modelling. Some form of grant / subsidy would also be required – should this not be possible, land would need to be secured at zero value for affordable rent or at minimal land value for shared ownership which will require “muscular planning policy and strong Section 106 agreements, based on a realistic growth-oriented approach to viability testing of policy.” Other challenges of stimulating housing output in this manner include land availability (competition with private developers and the market is dominated by 11 large housebuilders); skills shortages across the development production chain; regulatory concerns (cautious stances by the Housing and Communities Agency and downgrading risks); misjudging the housing market and greater exposure to cycles should grant / subsidy provision dissipate.

Wren Laing, Area Manager at the Greater London Authority (GLA) went on to reiterate the London Mayor´s pledge to raise the supply of affordable housing, regardless of the economic and political impacts of Brexit. The GLA will aim to bring more certainty by means of the “Homes for Londoners” Supplementary Planning Guidance (published at the end of November 2016 and under consultation until 28th February).

With London receiving £3.15 billion (announced in the Autumn Statement), the GLA has an unequivocal responsibility to widen the diversity and flexibility of affordable products; build its Innovation Fund; boost supported housing and “move-on” accommodation supply and adopt clear strategies on investment in housing infrastructure.

Adopting a “threshold” approach, affordable housing provision will be set at 35%; trader developers that can achieve this without subsidy will not be required to provide viability information and will be unlikely to have review mechanisms. Laing acknowledged that even with the Help to Buy equity loan scheme funding 1/3 of purchases and historically low interest rates, many Londoners still cannot save enough – resulting in the need to not only develop the PRS sector more resolutely but also help those that want to get on the ladder. With London rents rising by 10% per annum, inhibiting many young people´s ability to save, Laing claimed that the London Living Rent can serve as a pathway to Shared Ownership and eventual full ownership. Relieving the temporary accommodation pressures, effectively implementing the London Affordable Rent model and the recently announced £50 million budget to tackle homelessness are all being viewed as priorities.

One of the last presentations of the day by barrister Richard Humphreys QC of No. 5 Chambers summarised that there will be little immediate change to planning rules derived from European laws. The Great Repeal Bill of the European Communities Act (ECA) will take effect on the day of Brexit (two years after Article 50 of the Lisbon Treaty is invoked). Any pre-Brexit implementation would place the UK in breach of its EU Treaty obligations. Commenting that “there is not going to be an immediate bonfire of regulation,” Humphreys explained that UK law will not be removed from EU law and there will be a “disentanglement” process of many thousands of provisions. “Nothing is going to fundamentally change overnight,” he commented and EU law will remain UK law on Brexit day – then, over time, the relevant parts will be repealed. Nonetheless, citing the Conservation of Habitats and Species Regulations of 2010, Humphreys mentioned that some laws may well be interpreted differently during the negotiation period, particularly where there are questions related English-language semantics. This in turn could make court-decisions more complex, thereby requiring modifications over time.