The following collection of property expert commentary delves into a range of topics moving into 2019.

Rolled out for the second year (see the 2018 version), perhaps unsurprisingly, Brexit’s impact on the market remains a common theme. Yet, while gauging the exact effects is anyone’s guess, the underlying mantra of ‘keeping calm and carrying on’ prevails across this year’s contributions.

This is not to understate the risks. Potential interest rate hikes, negligible capital growth (at best), affordability constraints, and the wind coming out the sails of London’s global hub status are a handful of factors that could spell danger for the over-exposed. For landlords, the tightening screws resulting from Section 24 and ever-higher barriers to entry continue to shake-up the industry for the worse. 2019 is also likely to be a testing year for emerging operators in the build-to-rent, property crowdfunding, online house sales and lettings sectors.

But where there’s panic there’s opportunity. The demand for housing – owner-occupied and rental – shows little sign of abating. Savvy investors will adapt to the cycle’s positioning accordingly and look to reap the benefits of a buyer’s market in the event of a downturn.

To automatically scroll to the specific commentary link of your choice, click on the links in the drop-down contents box above. You’ll also see an arrow towards the right which can be used to return to the top of the post.

The Property Investor’s Blog would like to thank all contributors for their extensive input. It’s genuinely appreciated and we’re sure the content will serve readers well as 2019 progresses. Please feel free to send over your comments and thoughts to ruban@psinvestors.co.uk.

Chief Economist at the Royal Institute of Chartered Surveyors (RICS), Simon Rubinsohn

, Simon Rubinsohn") “Housing market activity set to weaken again in 2019: The UK residential market has continued to struggle against several well-established obstacles over the past year. Affordability issues, a lack of stock, political uncertainty and the prospect of further interest rate rises have all been factors seemingly weighing on activity to varying degrees.

“Housing market activity set to weaken again in 2019: The UK residential market has continued to struggle against several well-established obstacles over the past year. Affordability issues, a lack of stock, political uncertainty and the prospect of further interest rate rises have all been factors seemingly weighing on activity to varying degrees.

Sentiment has remained relatively subdued as a result, with new buyer demand tailing-off gradually throughout much of 2018. Sales volumes have also weakened during the past twelve months, while house price inflation has continued to cool at the national level. In the near term at least, we remain unconvinced that activity trends will break away from the recent sluggish picture.

Nevertheless, tackling the challenge around supply and affordability remains a primary goal on the domestic political agenda, with the prime minister announcing a scrapping of the local authority lending cap for housebuilding in the latest attempt to boost delivery. Just how effective the policy measure will be in lifting housebuilding remains to be seen, but, either way, the government still faces a huge task in reaching their 300,000 new homes per year target 2022.

Rental growth to accelerate slightly: The challenge around supply is no less of a problem on the lettings side of the residential market, with policy changes in recent years not helping in this regard. The additional Stamp Duty surcharge payable for buy-to-let investments has certainly had a lasting impact on slowing numbers of landlords entering the market.

Furthermore, the phasing out of mortgage interest relief, with further reductions still to come over the next few years, is also being factored into investors’ decisions. As it stands, the RICS indicator tracking landlord instructions coming to market has already been in negative territory for ten successive quarters. This is the longest stretch of declining supply in the rental market since the series began in 1999.

On a more positive note, according to the British Property Federation, institutional development of purpose-built rental properties has picked-up. The number of completed build to rent units increased by 26% in the twelve month to Q3 2018, now standing at 26,000. The pipeline going forward also appears strong, with construction underway on a further 42,000 units while 64,000 are in planning. That said, considering there are an estimated 4.6million households in the private rented sector, these numbers remain on a pretty small scale.”

Simon Rubinsohn @RICSnews – Chief Economist, Royal Institute of Chartered Surveyors (RICS)

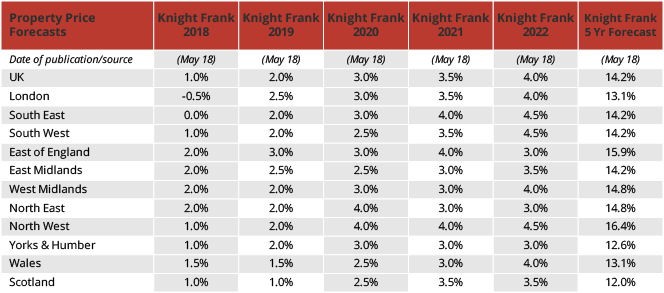

Partner and Head of UK Residential Research at Knight Frank, Gráinne Gilmore

“The political uncertainty thrown up by the lack of clarity around the UK’s future trading relationship with the rest of the world is having ramifications in all UK sectors, not just property.

“The political uncertainty thrown up by the lack of clarity around the UK’s future trading relationship with the rest of the world is having ramifications in all UK sectors, not just property.

However, when looking to the future, the Brexit noise can threaten to drown out everything else. It is worth putting in some earplugs to examine the other fundamentals of the housing market, as they will determine what happens in the years to come, once the Brexit dust settles.

Affordability, for example, is a key issue. Average house prices are around 22% higher than at the previous peak of the market in late 2007, but, in London, prices are 60% higher. In the South East, average values are 37% higher. This growth in house prices has pushed the ONS’s measure of affordability (house price to median residence-based earnings) to 13.2 in London, up from 8.4 in 2007.

The sales market has been thrown into sharper focus by slowing activity in some parts of the country. It’s no less of a factor in the rental market, however, where policy changes for landlords are affecting demand and supply dynamics, and pricing, in some parts of the UK.

The housing market, as with all markets, can absorb and adjust to change. Uncertainty is the most challenging factor of all, so sooner is better when it comes to a Brexit outcome.”

Grainne Gilmore @ggilmorekf – Partner and Head of UK Residential Research, Knight Frank

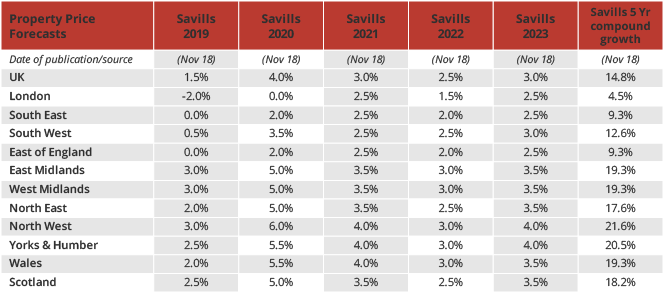

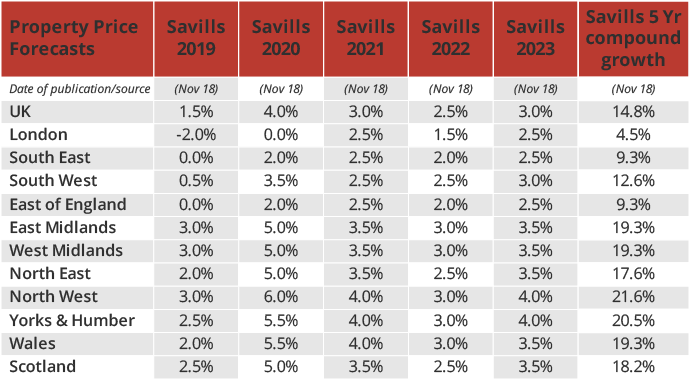

Director of Savills Residential Research, Lucian Cook

“Brexit angst is a major factor for market sentiment right now, particularly in London, but it’s the legacy of the global financial crisis – mortgage regulation in particular – combined with gradually rising interest rates that will really shape the market over the longer term. That legacy will limit house price growth, but it should also protect the market from a correction.

“Brexit angst is a major factor for market sentiment right now, particularly in London, but it’s the legacy of the global financial crisis – mortgage regulation in particular – combined with gradually rising interest rates that will really shape the market over the longer term. That legacy will limit house price growth, but it should also protect the market from a correction.

On London: House prices have risen by 72 per cent over the past ten years, well ahead of any other region. The average home buyer with a mortgage now pays just under £429,000 and has a household income of almost £76,000 (58 per cent higher than the UK average). Even with borrowing at over four times that income, these households still need a deposit of £123,000.

Small falls (-3.5%) are expected in London’s mainstream market next year, before values bottom out in 2020 and tick up steadily from 2021. Price growth over the next five years is forecast to total 4.5 per cent.

The prime London markets are less dependent on mortgage borrowing and will outperform the mainstream. The UK capital is expected to remain an attractive place to live, work and own residential assets, supporting12.4 per cent price growth in prime central London by the end of 2023.

On the Regions: At this point in the cycle, the highest price growth is expected in the lower value markets much further from the capital, which have seen nothing like the 10-year price rises seen in London – just 1.9 per cent in the North and 5.8 per cent in Scotland.

The Midlands, the North of England, Yorkshire and Humberside, Scotland and Wales all have the capacity for borrowing to increase relative to incomes, even allowing for higher interest rates, and this will support price growth ranging from 17.6 per cent to 21.6 per cent across these regions.

Key regional economies – most notably the metros of Manchester and Birmingham – have the capacity to outperform their regions attracting both local and investor buyers.

Wales will perform in line with the Midlands as it has done in previous cycles, but it is a hugely diverse market. There may be increased housing demand crossing over from Bristol once the Severn bridge tolls are abolished.

Scotland, which has only recently returned to pre-credit crunch peak, is performing strongly, particularly Edinburgh and Glasgow, which have seen prices rise 8.9 per cent and 7.0 per cent over the past year, respectively.

Rental Market Trends: Rental growth is expected to track house price growth, averaging 13.7 per cent over the next five years. Tightening access to mortgage finance and limited social housing supply is driving demand for privately rented homes at all price points. This is particularly true in London, where rents will rise by 15.9 per cent.

Until the market sees a significant injection of build to rent stock, rental demand will outstrip supply and rents will rise. Investor buyers requiring borrowing are expected to focus on higher yielding markets and this will put further upwards pressure on rents in some of the most expensive rental locations.

Transactions: Transactions have fallen from 1.619 million in 2007 to around 1.145 million this year, but are forecast to remain stable over the next five years, though the market mix has changed.

Cash remains king and cash buyers now account for almost a third of all sales (31%). The bank of mum and dad has provided important support to first-time buyer numbers and, judging by receipts from the three per cent surcharge for additional homes, cash is also an important component of investment demand, Savills says.

Mortgaged first time buyers, the only buyer group to have expanded since 2007 – from 359,000 to 370,000 this year – continue to be supported by Help to Buy and the bank of Mum and Dad. Numbers are expected to remain robust despite the prospect of a less generous, more targeted Help to Buy, with a fall of just -2.7 per cent anticipated by 2023.

Mortgaged home mover numbers have fallen dramatically since 2007 as existing home move home less frequently. Numbers are down from 653,000 to 370,000, but having adjusted for stress testing of borrowing, are expected to remain constant over the next five years.

Buy to let buyer numbers will continue to come under pressure. Stamp duty and mortgage-interest tax relief changes have led highly leveraged investors to rationalise portfolios or pay down debt.”

Lucian Cook @LucianCook – Director Residential Research, Savills

Property Expert, Henry Pryor

“Things are going to get worse before they get better. In Q1, the run-up to our actual divorce at the end of March there will continue to be people who have to sell. Death, debt and divorce – the three D’s as we call them in the industry will continue to drive the sale side but how many people ‘must’ buy? The only ones I think who will be confident doing so will demand something for the risk they will think they are taking which in most cases will be a discount on the price. Housing market statistics are based on deals done three or four months earlier, on average 60 days before the sale completes so regardless of whether we crash out on 29th March or enter a new golden era the statistics in May, June and July will show prices falling. This may result in buyers panicking that prices are still falling after Brexit resulting in more uncertainty and the cycle gathering its own downwards momentum.

“Things are going to get worse before they get better. In Q1, the run-up to our actual divorce at the end of March there will continue to be people who have to sell. Death, debt and divorce – the three D’s as we call them in the industry will continue to drive the sale side but how many people ‘must’ buy? The only ones I think who will be confident doing so will demand something for the risk they will think they are taking which in most cases will be a discount on the price. Housing market statistics are based on deals done three or four months earlier, on average 60 days before the sale completes so regardless of whether we crash out on 29th March or enter a new golden era the statistics in May, June and July will show prices falling. This may result in buyers panicking that prices are still falling after Brexit resulting in more uncertainty and the cycle gathering its own downwards momentum.

I don’t think that the housing market is going to test the Bank of Englands models by crashing by 30% but I do expect prices to slip by 10-15% – the discount that most buyers I imagine will demand if they are going to commit to what for most will be their most expensive single purchase. Savvy sellers will need to remember that they can make up for this by negotiating similar discounts on what the go on to buy.

As always there will continue to be regional disparity, prices in some parishes will rise whilst others will fall further. As Phil & Kirsty remind us, it’s about location, location, location. Best in class will always sell and will always be sought after.

London and the South East have seen the real house price growth over the last decade, they stand to lose the most but I expect rental prices to slide back too. Brexit is just one iceberg that we need to navigate a way past in 2019 – politics, the economy and confidence, in general, will all have a significant part to play on prices. If I’m honest, I don’t know what’s going to happen to prices in the medium to long term but one thing you can be confident of is that a house will always be worth one house.”

Henry Pryor @henrypryor – Property Expert

Land, Planning & Development Expert and CEO at Millbank, Paul Higgs

“In terms of my personal approach, I’ve always been risk averse and detail orientated – which is fundamental in property development as it really is a super risky business, even at the best of times. With any deal, I spend a lot of time researching every aspect thoroughly and exploring all the exit options given various scenarios. Ultimately, I want to create maximum value from the start and a decent ‘buffer’ regardless of where the market is heading.

“In terms of my personal approach, I’ve always been risk averse and detail orientated – which is fundamental in property development as it really is a super risky business, even at the best of times. With any deal, I spend a lot of time researching every aspect thoroughly and exploring all the exit options given various scenarios. Ultimately, I want to create maximum value from the start and a decent ‘buffer’ regardless of where the market is heading.

Over the last few years, I’ve taken an even more cautious attitude to anything I want to get involved with. Obviously, no one can predict the market or know what’s really going to happen – but as I’ve been through a few crashes, I’m well aware of the signs, potential triggers and where things might end up.

Prior to the Brexit vote, for example, I suspected that if we did vote to leave there would be a great deal of uncertainty in the market. The market obviously hates uncertainty and in development everything is exacerbated further because of the long timescales involved in the process. I didn’t want to be in the middle of building and selling if the vote was made to exit, or worse still when the time approached to actually exit – i.e. now. As a result, for the past couple of years I’ve been focusing on adding maximum value to land, which is always my strategy actually, but with a view to flipping sites with planning rather than holding them to build-out.

London and South East prices have plateaued for the last year and a half in reality so I’ve also been a bit more involved helping-out JV Partners on bigger sites in areas like Birmingham, Liverpool and Leeds, where the market has largely continued to move in the right direction.

Obviously the more traditional strategies like buy-to-let have become harder (due to the SDLT changes, Section 24, increased regulation etc.). As a result, many property investors have shifted into development thinking it’s the ‘next best thing’.

What’s often forgotten is that property investment and property development are massively different things. People think that if they have been in property for a while and maybe have a large portfolio of single lets or HMOs, then jumping into development makes logical sense when, in fact, there’s a very steep learning curve.

As a result, there have been lots of new entrants coming into the development space in recent years who are buying sites on the market, bidding too much, overpaying and generally getting their figures wrong. Often, people can get into a mess and the market comes to the rescue. But where we are now in the market, many of these people won’t be so lucky. These questionable deals are starting to hit the market and come to light. The units are not selling for as much as originally hoped or quickly enough. With highly-leveraged deals some funders having already started pulling the plug. My expectation is that these trends will continue big-time into 2019.

Therefore, my advice is to be careful who you listen to as many out there really do not have the necessary experience to get involved in what is a complex business. Property development can be very high-reward because it’s very high-risk.”

Paul Higgs @Paul_Higgs1 – Land, Planning & Development Expert at Millbank Land Academy and CEO at Millbank

CEO at Inspired Asset Management and Inspired Homes, Martin Skinner

“We expect 2019 to continue in the same vein as it is currently until Brexit is resolved. Whilst we remain confident the UK will agree a deal, as long as there is uncertainty, some buyers will postpone their purchase. Once a deal is struck, we expect confidence to return to the market, however, price growth will be moderate, linked to wage growth, as the market continues to be owner occupier rather than investor led.

“We expect 2019 to continue in the same vein as it is currently until Brexit is resolved. Whilst we remain confident the UK will agree a deal, as long as there is uncertainty, some buyers will postpone their purchase. Once a deal is struck, we expect confidence to return to the market, however, price growth will be moderate, linked to wage growth, as the market continues to be owner occupier rather than investor led.

2019 will most likely continue to be a buyer’s market and competition between developers will mean there are deals to be had such as solicitors fees paid and free furniture packs. For this reason, and with mortgage rates still very low, it’s actually a good time to buy if you’re an owner occupier.

If you’re a first-time buyer, you’ll also benefit from zero stamp duty on the first £300,000 of a purchase up to £500,000, meaning you’ll only need your 5% deposit to become a homeowner when using Help to Buy.”

Martin Skinner @MartinSkinner – CEO, Inspired Asset Management and Inspired Homes

Founder and Director at the TrustedLand Directory & The Developers Boardroom, Alex Harrington-Griffin

“In terms of land and planning, there is no doubt that access to quality site opportunities around the South-East has was a struggle in 2018, as most vendors without motivation that had access to the outside world will know that if they’re looking for best returns, they won’t get it now. Therefore, I certainly expect a dramatic shift, as we pass through Brexit and banks tighten purse strings, that site acquisition strategy, and type, adapt dramatically for forward-thinking and astute buyers.

“In terms of land and planning, there is no doubt that access to quality site opportunities around the South-East has was a struggle in 2018, as most vendors without motivation that had access to the outside world will know that if they’re looking for best returns, they won’t get it now. Therefore, I certainly expect a dramatic shift, as we pass through Brexit and banks tighten purse strings, that site acquisition strategy, and type, adapt dramatically for forward-thinking and astute buyers.

More distressed site purchases, more developer-developer and landowner-developer Joint Ventures to mitigate risk and embrace transparency. I expect small and medium land buyers will be looking at areas of the market and site variations not previously considered, creating products that are somewhat out of their usual remit, or that break the mould in terms of design and style, to ensure that their product stands out and certain buyers will pay extra for that unique product.

The widespread adoption of technology and mapping tools by both experienced and new developers to access land opportunities is growing rapidly, with buyers taking it upon themselves to contact owners. However, the smart ones will listen to vendor feedback in terms of the volume of contact, and start to consider innovative ways to help their brands and bids stand out, and hopefully use transparency and trust to win opportunities, through collateral and open book appraisals. The world is becoming more transparent, not less, and a lot of vendors are now wise to this and what they can find online.

Finally, I would expect we see a move by SME resi developers, in line with the monthly discussions held within Developers Boardroom, into areas such as build-to-rent, retirement, co-living, micro-flats and even industrial/commercial, as established teams look to utilise their skills and experience in emerging active sectors where a long-term potential, such as baby-boomer accommodation, and to be looking at longer-hold, cash flowing asset creation.”

Alex Harrington-Griffin @Alex_H_Griffin – Founder of the TrustedLand Directory and Director at Developers Boardroom

Managing Director of the Property Developers Academy, Brynley Little

“2018 saw the market softening in many areas in the UK which triggered the acquisition phase for those experienced within the land and new build sector. This will firmly continue into 2019.

“2018 saw the market softening in many areas in the UK which triggered the acquisition phase for those experienced within the land and new build sector. This will firmly continue into 2019.

Uncertainty and a softening of the market has reinforced our focus of acquiring sites for both socially and locally affordable homes. Affordability is a growing issue in many areas and working with Local Planning Authorities to combat this issue could see great relationships built and great deals to be done.

Sites with high value properties continue to carry a large amount of risk in the current climate. They are becoming less desirable for experienced developers and funders alike. ‘Modular’ certainly seemed to be the buzzword in development in 2018, and I’m sure it will continue to be spoken about throughout 2019. Will 2019 see Modern Methods of Construction gather significant pace from a delivery point of view rather than the spoken word, I’m not so sure. There is still a way to go for modular homes to displace traditional methods in my opinion.

There are two growing trends to be aware of that I believe will open up opportunities and potentially bring focus to those looking to either start or scale their new build business in 2019; The Rise of the Millennials and the Coming of Age of the Baby-Boomers. These two demographics represent opportunities for increased rental demand, affordable homeownership and downsizing to more appropriate accommodation.

My recommendation for 2019, if you haven’t already, is to shift your focus to acquiring land and obtaining planning for deliverable schemes for both the rental and affordable for sale markets.”

Brynley Little – Managing Director of the Property Developers Academy and Co-Founder of Your Land Partner

Director of Real Estate Policy at the British Property Federation, Ian Fletcher

“It looks like we are going to start 2019 with the same Housing Minister in post. Possibly wishful thinking, given so many political scenarios that could unfold as a result of Brexit, but we sense a steely determination on Kit Malthouse’s part to hang around, and a wish to stop the housing minister merry-go-round.

“It looks like we are going to start 2019 with the same Housing Minister in post. Possibly wishful thinking, given so many political scenarios that could unfold as a result of Brexit, but we sense a steely determination on Kit Malthouse’s part to hang around, and a wish to stop the housing minister merry-go-round.

The overall supply of new homes will likely reach 240,000 homes annually – once seen as a significant milestone, but now just a stepping-stone towards 300,000 homes per annum. In addition to much-needed firepower behind other housing sectors, I am fairly confident several big Build-to-Rent transactions will take place in 2019, as larger institutional investors seek to acquire a piece of the action.

Brexit will continue to overshadow the Government’s domestic legislative programme, with several big issues in the housing sector requiring legislation – leasehold reform, implementation of the Hackitt Review, single ombudsman – getting delayed. And, council house building will get off to a slow start, hampered by a lack of skills and capacity. There will also be a stiff test of the Government’s financial credentials as the Chancellor conducts his spending review. Council finances will be a big issue, as several local authorities can cut no more.

And, for the cherry on the cake, I’m going to hazard a guess and say an independent high-profile contender will throw their hat into the ring for London Mayor.”

Ian Fletcher @BritProp – Director of Real Estate Policy, British Property Federation

Founder & CEO at Realyse (Housing Market Intelligence), Gavriel Merkado at Realyse

, Gavriel Merkado at Realyse") “How to predict the future in an uncertain world

“How to predict the future in an uncertain world

Time and again I find myself being asked: What about the future? What can you tell me about what will happen tomorrow? Next week? Next month? Next year? In this article we’ll play the dangerous game of plotting the future course for the UK market – breaking down the key factors that will have a significant impact on housing prices in 2019.

Before we get started however, it’s worth exploring exactly why trying to see into the future is so problematic, and why using a rational approach can lead to better (and far more likely) predictions grounded in data. Foresight of coming events used to be so valuable that in ancient Greece the Oracle of Delphi could lay claim to being the most powerful woman in the world.

When a vast Persian army invaded Greece and the Oracle was consulted for guidance, she told the Athenians to “trust in a wooden wall.” Personally, I would have gone out and built a big fence, but instead this was interpreted as an instruction to construct a fleet of wooden ships. As a result, history took a different course, and the Persians were halted.

This highlights the problem with attempting any forecast; the sheer complexity of the present moment. The endless number of different variables that can have a bearing on every possible outcome, even in systems that are governed by determinism and clearly quantifiable principles, make them near impossible to predict. The mystery element is what fascinates (and frustrates) us when considering the future.

Let’s start with a simple example. You could forecast that if you were holding a ball, and then decided to let go of it, the outcome would be the ball falling to the ground (thanks gravity!) and anyone could pinpoint with great precision where the ball will land.

Now, try throwing the ball at a specific point on a wall. The distance, time and angles of movement all start to confound the accuracy of where it will actually hit. Harder to say for sure if it’ll land perfectly every time. Finally, try throwing that ball, into the wind, with a thousand other people all throwing balls at the same time. Some argue that the majority of forecasts are unreliable because the past cannot be used to predict the future in a meaningful way, because the elements are a Markov process. However I don’t consider that to be the case when human psychology is an active part of the process.

The value of any forecast is a function of the deviation from the actual, the time span and the perceived value it has for the recipient of the forecast (usually monetary). So if we return to our earlier example, telling you with absolute certainty that the ball I dropped is going to land on the floor in one third of a second, has almost no value at all.

Telling you that the ball I dropped now, in the year 2317, is going to roll under the left wheel of the future robot king and cause it to catastrophically malfunction, is actually also pretty much worthless, for a different reason. Because of the finite nature of the human lifespan, we often devalue long term forecasts, much to the chagrin of many environmentalists.

But, we digress. I have been asked to forecast the relatively near-term future, of house prices, here in the UK and for 2019. So, firstly, some definitions and ground rules:

House prices – The median price change of residential property, in aggregate, not weighted by value. So if a £1m house goes down 10% and £100k house goes up 10%, the median change is 0%, not -9%.

The UK – All of what is currently considered the UK at the time of writing, regardless of what happens with any EU issues around Northern Ireland and Scotland.

2019 – January 1st, to December 31st.

What do we know about the largest inputs which will be affecting our forecast?

From a Macro perspective: Interest rates and credit availability, global economic growth (or decline), auto-correlation of activity, inflation, UK economic growth, supply & demand.

From a Micro perspective: Individual expectations of housing markets, pricing, and macro factors, as well as changes in fashion, personal wealth etc…

Interest Rates & Credit

For the past ten years there’s been talk of the Bank of England raising base rates, and then finally it happened towards the end of 2017. The forward curve has been upward sloping for almost as long as I’ve been looking at it, so just because there is an ‘expectation’ of rising rates, doesn’t mean anything, as the expectation has been there for the past decade and hasn’t happened. What it will come down to, like so many other things in the near future, is what happens once the UK leaves the EU.

If there is a poor economic situation following Brexit, it may result in immediately lower rates in the UK, even negative rates (as have existed now in Europe for several years) as the Bank of England aims to improve the economic environment. Conversely, if there is a run on the currency, then the BoE may choose to raise interest rates to stop the depreciation, as was done in 1992 during the ERM crisis.

In a muddled-deal situation, with some kind of halfway house of the UK/EU not being entirely resolved, it is likely that rates would stay around the same level or slightly increase, dependent on the global economic environment.

In a good economic situation, following the UK leaving the EU, whereby either the UK gets a good deal from the EU or quickly creates favourable new deals with other significant trading partners, rates may actually increase.

Similarly, credit availability will likely be impacted by the outcome of Brexit votes, with a poor economic situation leading to looser credit availability and perhaps even returning to QE.

Overview – Rates remain the same.

Global Economic Growth

What is interesting beyond the political mire of the ongoing spat between the UK and EU is actually the changing financial and economic characteristics of the rest of the world around them. While the majority of the EU has been lagging far behind, the UK has over the past few years been returning to some sense of economic well-being. Meanwhile, the US has been steaming ahead. Markets are up, interest rates are up, growth is up, incomes are up. The US is now in the second longest ‘bull run’ in history.

However for a variety of reasons, US yield curves briefly inverted last week, a tell-tale sign that moods are shifting and the party may well be over in a year or two. As the world’s largest economy, when the US sneezes, the world catches a cold. While it is slightly outside the scope of this one year forecast it is worth keeping any eye on what happens across the Atlantic in 2019.

In the world’s second largest economy, China, we know growth is slowing, power has become even more centralised in Xi Jinping (creating decision risk) and the enormous debt taken on by the corporate sector (total debt in China is now equivalent to 300% of GDP) increases their economic risk weighting. The UK’s recent relative currency weakness does potentially create a nice buying opportunity for overseas buyers, if they believe there is more economic upside in the UK.

Why is this relevant to us? Keep in mind that a large proportion (if not the majority) of buyers of newbuild properties in major cities UK are overseas buyers, and that demand from those foreign buyers has been largely supporting the current price levels of new property developments. If those buyers go, because of changes their local economies, the support for the high prices in the UK goes along with them.

Overview – Slower growth globally

Auto-Correlation and a buyers market

Have you ever noticed how people talk about ‘property prices going up’ in an area, and there’s some kind of palpable excitement to it, like a panhandler telling you about a fresh seam of gold they’ve just heard about up yonder? Word of mouth spreads, and other people start buying in the same area, hoping to get in on the wave of price increases while they still can, this pushes prices up further, encouraging the next batch of people to buy in before it’s too late.

The same buying behaviour can be seen whether it’s in houses, cryptocurrency or the latest fashion sales. Property prices are auto-correlated, and because of this we can often predict that the future will closely resemble the present. What we’ve seen over the last year is a significant decrease in the volume of transactions. The uncertainty around Brexit, and the already extremely high prices in many parts of the country, as well as secondary impacts from changes in stamp duty and the changing dynamics and spending power of overseas buyers have all led to reduced volumes overall.

These reduced volumes are likely to continue until such time as something significant changes in the political and economic environment, which gives people more clarity on what the immediate future may be like. The housing market in Australia is currently going through this period of auto-correlated decline now, having gone through an extended period of price increases. People there are now waiting for the market to bottom out, but it’s expected to continue to decline by a further 10%, so they keep on waiting. Lower volumes doesn’t necessarily create a directional impact on the market, although some would claim that it does.

As every transaction must have a buyer and a seller, all that a lower volume of willing buyers and sellers does is to push pricing in favour of either the buyers or the sellers overall, depending on which group is more desperate. The likelihood is that someone who needs to sell, needs to sell, they have to do it. For example, the seller has to pay their inheritance, alimony, move to somewhere else etc. Yet there is no such thing as someone who needs to buy, since you can always rent, or find somewhere else.

In a market with fewer deals going on, the impact of the desperation of sellers, can over time, cause them to drop prices well below what they would previously have accepted.

Overview – Expect low volumes to remain, and for that to push down on prices.

Inflation

Ever hear of stagflation? Its when you get a low or negative growth economy, coupled with high inflation, effectively the inverse of the normal economic relationship. Usually inflation follows real growth, growth goes up, and then so does inflation a little later, and then in theory central banks use interest rates to control growth and thereby limit inflation, or at least the expectation of inflation.

However, you can have a situation where there is low growth but rising inflation, where you’re paying more for the same thing (inflation) but the environment around you isn’t changing. It doesn’t happen very often, but when it does it’s caused by a shock external factor causing prices to rise. Well, how about a country leaving the world’s largest political/economic bloc as a shock? Exchange rates took the brunt of the impact of the referendum vote, resulting in higher import costs for the UK (and interestingly, putting a real quantifiable value on voting behaviour, but perhaps that’s another story).

If the economy continues to work ‘as normal’ in the coming year then inflation will simply be a factor of economic growth and commodity costs, which are not expected to be particularly high in 2019. However, if the exit from the EU creates further currency devaluation, then it could lead to higher inflation as the cost of imports rises. As inflation rises, people beginning to mentally price in that inflation will continue, causing them to change their buying behaviour and pricing, resulting in a spiral of unwanted inflation. Inflation makes it harder to price assets and commodities in real time, as if inflation is higher, the price of the asset may be changing faster than you can keep up, creating all kinds of inefficiencies, and often lowering the number of transactions. The Bank of England is also forecasting higher than ‘normal’ inflation for 2019 at 3.2%.

Overview – Possible negative risk, keep an eye on FX markets

UK Economic Growth

There are a great many pundits and think tanks out there making economic forecasts, usually picked up on by news outlets depending on their own particular political bias. Some come from very important sounding organisations, and most forecasts are usually wrong. As we’ve shown, it is incredibly hard to make an accurate forecast of a complex system where the majority of parts are unknown and the relationships between them can often only be guessed at.

However one organisation I believe has come closest to proving itself accurate more often than not is Oxford Economics. Their forecast for 2019 in 1.5% GDP growth in the UK, which is somewhere between 2017 and 2018 results. So the expectation is that next year will be somewhat like this year and the year before. It could be that a no-deal situation in Brexit results in import and export tariffs, increasing both the cost of purchases of EU stat products in the UK and the cost of EU states purchasing UK products, that may be offset by opening up the UK to greater trade with the rest of the world. Conversely a trade deal with the EU could maintain the status quo.

Overview – No change

Supply & Demand

The official population of the UK is c.66M, however it may well be higher, and according to government statistics there are 25 million homes (although our own figures show a higher number). So there are 2.6 people per house in the UK. Germany for comparison comes in at 2.2 people per house, the USA at 2.4 and Japan, (often characterised by very tight living conditions in its major cities) at 2.5 people per house. Of course there may be different styles of living in those countries, for example people living with their parents longer, or demographics resulting in smaller family units (which i’m not taking into account) this is simply a guide.

So it would appear that the UK is undersupplied in housing by at least 4% (if we want to catch up with Japan), if not more likely 10%-15% (if we want to catch up to somewhere near the USA or Germany). Which is roughly equivalent to either 1 million more homes, or 3.75m depending on which comparison you prefer.

The UK is currently building ~200,000 new homes per year, although the average over the past few years is closer to ~150,000. So it would take at a minimum, assuming a constant population level, five years for supply to meet demand. In reality, the population of the UK is increasing by about 400,000 people per year, so all of those new houses are actually going straight to new additions to the population.

Realistically for supply to meet demand, the UK, over a five year period based on the persons per house found in other countries, would probably have to produce close to 800,000 new homes per year over five years, or 400,000 over ten years. This is unfortunately very unlikely – in fact almost guaranteed – not to happen.

So supply is constrained, however so are incomes, thus the only logical choice for prospective home buyers is to either move further afield from their place of work (maybe buy transportation stocks?), or to rent instead. Additionally, the uncertainty around the housing sales market may encourage some people to either continue renting or start renting rather than risk a poorly timed or unaffordable purchase.

Overview – Strong positive for ‘commuter towns’ and central renting locations, negative for central sellers.

Individual Expectations

This is a tricky one to understand, however sentiment can often drive markets just as much as, if not more so, than fundamentals. Individual sentiments and expectations, in aggregate create economic action. So what are those individuals expecting? Looking at the PMI (purchasing managers index) and the CCI (consumer confidence index) shows that while both are down somewhat over the year, neither is in a particularly different position to where it has been over the past couple of years. So the expectation in that sense is that next year will be much like the past couple of years.

Overview – No change

Personal Wealth & Income

Why have property prices gone up in the past half decade? Did everyone suddenly get a lot richer? Did the population increase exponentially? Did half the supply of houses in the country disappear? Nope, two things happened, interest rates fell, and lending increased. However, at the same time, banks changed their lending requirements, generally forcing a requirement for higher deposits. Meaning that housing became very much dependent upon the ability to raise a deposit, and this was often found from the equity held in a property that is already owned.

While on average people have gotten somewhat wealthier, it hasn’t been by much, and arguably a large portion of the population isn’t better off than they were a decade ago. Recent economic figures don’t indicate that this trend will change, with some recent metrics marginally positive and others marginally negative, effectively cancelling each other out.

Meanwhile, the income-to-price ratio of most residential properties has already reached, or is in excess of, the maximum sustainable level. With that in mind I don’t see a huge change resulting from personal wealth and income over the year that lies ahead.

Overview – No change.

Summary Overview

To sum up, we have the following results:

| Factor | Impact on prices |

| Personal Wealth & Income | No Change |

| Individual Expectations | No Change |

| Supply & Demand | Positive for rents, commuter towns, negative for central or high price locations |

| UK Economic Growth | No Change |

| Inflation | Possible negative |

| Autocorrelation | Slight negative |

| Global Economic Growth | Slight negative |

| Interest Rates & Credit | No Change |

With all of the above in mind, I believe that the UK will see a mixture of different results depending on the location and property type. However in aggregate we’ll see modest price and rent increases primarily driven from the supply/demand imbalance, but constrained by limited changes in personal wealth and downward pressure from macroeconomic factors.

Let’s see what happens in 2019, who knows, I might actually be right!”

Gavriel Merkado @REalyse_UK – Founder & CEO, Realyse

Senior Economist at the Construction Products Association, Rebecca Larkin

“Noticeable variations in regional performance have emerged in the UK housing market over the last 12 months and this is a dynamic that is expected to go on into 2019. The strongest price growth is likely to continue in the North West, the Midlands and Yorkshire & Humber, whilst price falls in London ripple out to the neighbouring South East and East of England.

“Noticeable variations in regional performance have emerged in the UK housing market over the last 12 months and this is a dynamic that is expected to go on into 2019. The strongest price growth is likely to continue in the North West, the Midlands and Yorkshire & Humber, whilst price falls in London ripple out to the neighbouring South East and East of England.

Regional price growth, the Help to Buy equity loan and a dearth of pre-owned properties on the market have led to an increased role for new build, which now accounts for 14% of property transactions. This has been further complemented by house builders’ offerings being accompanied by a wider variety of tenures such as shared ownership and Build to Rent in response to longstanding affordability issues.

Perhaps the biggest theme for the near-term outlook, though, centres around developments in the political and economic landscape, which are currently the great unknown for builders, purchasers, investors and forecasters alike. The last recession showed us that a significant slowdown in the wider economy will undoubtedly hit the housing market and new build activity harder. On this front, the labour market, interest rates and appetite for mortgage borrowing and lending will be the key determinants of how the housing market progresses.”

Rebecca Larkin @CPA_Tweets – Senior Economist, Construction Products Association

PRS and Build to Rent Consultant, Richard Berridge

“2019: The Year of the Consumer Renter

I get a sense that the Build to Rent sector is getting just a little bit more mature. Those of us with genuine experience of institutional PRS, across a number of disciplines, are seeing a more considered approach to the development of schemes and a shying away of viability assessments based upon a premium above upper decile rents. Now, of course, we actually have real data to interrogate. Mirroring the collaborative approach of the US Multi-Family operators, some of the UK operators actually share this information. Some don’t. Old resi’ habits die hard.

In last year’s comment piece, I estimated that we could have close to 150,000 BTR units constructed, in planning or construction by the end of 2018. According to the British Property Federation, at the end of Q3 we have close to 132,000. Not bad going. Given there’s Q4 still to report on, I guess we could end up with 140,000. This demonstrates that not only have funds become comfortable with BTR, but actually desirous of it.

There’s little let up in the growth of potential investors either; Intu are reported to be considering repurposing the airspace above their retail portfolio (although sadly little understanding of the management paradigms seem to be evident) British Land are on the verge of creating a portfolio and we have seen Cortland enter the UK market with a £4bn war chest, aspirations to deliver 10,000 units, and the poaching of Andrew Screen from TradeRisks. So, from my perspective, Brexit or not, I expect 2019 to demonstrate stronger growth than 2018.

I would caution some new entrants against seeing BTR as simply a portfolio-balancing act. Watching institutions pour funds into new schemes might give prop-co’s the confidence to enter the market, but they need to take on board the learning that has been done in designing the asset for living and the quantum leap in management. It will not be enough unless the new thinking around quality, brand, customer service, environment, and wellness are employed and fully embraced. You can’t fake good BTR.

I’ve been a little disappointed in the rather prosaic nature of BTR marketing. Illustrated, perhaps, by not grasping the opportunity Black Friday or Cyber Monday offered. 2019 will see an acknowledgement that BTR is just another consumer product and we will see cross-market expertise from other industries drive innovative marketing and advertising. That will mean much more scientific use of demographic and psychographic data in harness.

I suspect 2019 will also see a wobble in Third Party Management. My discussions with a number of investors have revealed a cultural shift away from TPM and a desire to self-manage. This is going to create some difficulties and I would expect some high profile changes in management in the coming months and some creative JV structures between operational managers and investors.

Prop-tech hasn’t quite made the quantum leap I would have expected, except for one area: AI. In ‘general’ prop-tech (if there is such a thing) there’s been an awful lot of collaboration, much talking and some mild interventions in management. But AI is the game changer and we’re waiting to see who embraces it first. My feeling is that there will be some typical caution in implementation in 2019, and perhaps a little AI ‘light’ But I think it’ll be 2020 before we see anything really exciting. It’s always worth keeping an eye on Antony Slumbers for AI development. Data mining and interpretation from more operational schemes will become a priority. The data will be ‘richer’ and will highlight what renters really want and how it can be provided.

As last year, affordability is high on the agenda and rightly so. Whilst many planning authorities are BTR ambivalent, more, especially in London, are now looking for BTR to provide as many affordable units as OMS schemes. These will not just be DMR, as suggested in the NPPG, but will comprise a range of affordability levels. Our cousins across the pond are experiencing similar affordability issues. Last year, I posted a link to Harvard’s housing review that articulated concerns over affordability. This year’s Harvard ‘State of the Nation’s Housing’ review can be found here. Figures show that 80% of renters in the US are ‘cost burdened’ and that the numbers of renters have fallen by 180,000 to 43.1m. There are two factors at play here: cheap finance has seen an uptick in home ownership and, more worrying, younger cohorts are simply not forming new households. Many staying at home longer.

We see similar trends emerging in the UK. There is a growing concern that HA’s are not fulfilling their social purpose. Tom Murtha has been critical of this. Gradually starved of grant, HA’s have become vigorous commercial entities. Whilst not intrinsically a bad thing, there is evidence that the commercial side of the HA brain has taken precedence over the social-purpose side. However, I believe that this is now recognised and in 2019 and beyond I see HA’s taking the lead in developing major BTR schemes of blended tenure with a very strong emphasis on affordability and social-purpose. 2019 will also see a rise in flat sharing, driven by affordability, and for flat-sharing platforms to be embraced by some of the BTR operators. Ideal Flatmate is one such platform that I would expect to grow exponentially in 2019.

Yields: competitive, long horizon money has driven down yields across the country in 2018 with, no surprise, London sitting at around 4.75-5% gross or 3.5-3.75% net. With 10y UK gilts at around 1.2% (at time of writing) Institutional money is still sitting on an acceptable margin. Factor in rental growth over time and the picture looks better still. However, should we see interest rates rise, and Brexit could well be a factor here, yields will certainly soften. In any event, I would now be advising an increasing of yield factor by 25-50bps. Naturally, that would see a marginal fall in capital values.

Finally, BTR mustn’t lose sight of its key differentiator; peerless customer/user experience (CX/UX). There are some new players, Cortland for instance who understand this very well and will raise standards further. So, if 2018 was the year of the BTR investor, 2019 will be the year of the BTR renter as consumer consciousness finally becomes wide-spread.

Richard Berridge @ResiRichard – MLH-Investments: Institutional Residential Investment Multi-Family & Build-to-Rent

Head of PRS and Build to Rent at PRSim, David Bond

“With the ongoing demand for rental property, it was encouraging to see that during 2018 there was an increased focus on Build to Rent and institutional investment in the Private Rented Sector. This was acknowledged by the British Property Federation (BPF) who reported that the ever-increasing Build to Rent pipeline of units at the planning stage, or in construction, was in line to exceed 100,000 by the end of the year.

“With the ongoing demand for rental property, it was encouraging to see that during 2018 there was an increased focus on Build to Rent and institutional investment in the Private Rented Sector. This was acknowledged by the British Property Federation (BPF) who reported that the ever-increasing Build to Rent pipeline of units at the planning stage, or in construction, was in line to exceed 100,000 by the end of the year.

As we move into 2019, it is widely expected that these pipeline units will ‘hit the market’ and, with the support of institutional landlords, bring the much-needed stock to the sector and, it is hoped, satisfy the wide-ranging demands of tenants. As usual demand for apartments that are centrally located – with amenities close by – is likely to continue as is the need for single dwelling housing, perhaps near schools or local parks, for families. Added to this, however, there appears to be a growing acknowledgement that rental properties are needed for older tenants and those in the retirement sector.

A blurring of the lines between family housing – and later living – could, therefore, create a new interest in the rental sector for those semi or fully retired and who, to date, could see no transition between family housing and retirement/care living. The Centre for Ageing Better reported that, on the back of an English Housing Survey, a growing number of over 60s in the UK are renting and estimates that by 2040 a third of people aged over 60 could be living in private rental accommodation with demand for specialist retirement developments – with assured (lifetime) tenancies – potentially increasing.

For the institutional investors, therefore, it continues to be vital to understanding what tenants want – and where – and how they respond to this, whilst also, of course, considering what yields they may generate. The importance of developing strong relationships with national and regional house builders therefore remains and – even before a site is identified or planning application made – it’s crucial that an open dialogue between institutional investors and builders is maintained now and in the future.

Added to this, with the growth of institutional landlords, we are also seeing the wider use of deposit replacement schemes and PropTech playing a role in professional property management. The focus is on efficiency, performance and quality service to tenants with the ultimate aim being to help landlords retain them.

Housing has certainly been the focus of much debate during 2018 and appears to be firmly on the political agenda, but we must now wait and see what 2019 will bring and how, for the institutional landlord, and those people living in the Private Rented Sector, it directly affects them.”

David Bond @_PRSim – Head of PRS and Build to Rent at PRSim

Director at Just Do Property, Julie Hanson

“It seems highly likely that we will see a further softening of London house prices in the short term prior to the finalisation of any Brexit arrangement. The next two years could be challenging for London but experts believe that 2020 will see the cycle turn. Many have written off London as a ‘busted flush’ in times gone by only to see the market bounce back to take centre stage. Do not fall into that trap!

“It seems highly likely that we will see a further softening of London house prices in the short term prior to the finalisation of any Brexit arrangement. The next two years could be challenging for London but experts believe that 2020 will see the cycle turn. Many have written off London as a ‘busted flush’ in times gone by only to see the market bounce back to take centre stage. Do not fall into that trap!

The South of England, especially the South-East, will likely broadly follow the same path as London house prices in the short term. It is easy to forget these are areas of the country, the South-East in particular, which have significantly outperformed the rest of the UK (excluding London) over the last decade. Property investment is a long-term activity and while short-term fluctuations do obviously impact investor sentiment, the long-term trend is still your friend.

Infrastructure investment has also brought the Midlands and the North of England into play. The risk/reward factors compared to London are much more attractive and there is a feeling that investor sentiment is changing. However, once the dust settles on Brexit it would be foolish to dismiss a recovery in London prices in the medium to long-term.”

Julie Hanson @JustDoProperty – Director at Just Do Property

Director at Garrison Property Services, Adam Lawrence

“2019 looks like a year of considerable uncertainty as we look towards it in December 2018. We have definite activity in the UK next year – whether that be postponement of article 50, or a footrace towards a brick wall with a blindfold on March 29th 2019. The lack of skill displayed by the government in the past 12 months has truly been something to behold – if only spitting image were still around they would have had the most beautifully gift-wrapped bunch of satire, for real, delivered to their storyboards.

“2019 looks like a year of considerable uncertainty as we look towards it in December 2018. We have definite activity in the UK next year – whether that be postponement of article 50, or a footrace towards a brick wall with a blindfold on March 29th 2019. The lack of skill displayed by the government in the past 12 months has truly been something to behold – if only spitting image were still around they would have had the most beautifully gift-wrapped bunch of satire, for real, delivered to their storyboards.

A good place to start seems to be with predictions that I made at the end of last year for 2018, and see how they’ve stacked up – after all, you can then decide whether to scroll down or to bother continue reading! Here are my numbers from 12 months ago, and the actual results (numbers from land registry HPI):

- London market – capital values to be flat, best guess 0% – actual number -0.5%

- South-east England – flat/small growth, in the 1-2% region – actual number +2.04%

- Midlands regions – growth in the 5-7% region – actual number +4.15%

- North West – growth in the 3-5% region – actual number +4.5%

- Wales – growth in the 3-5% region – actual number +4.99%

- South-west – growth in the 2-4% region – actual number +2.78%

- North-East – growth in the 2-4% region – actual number +1.04%

So, overall, very pleased with that. A difficult year and I was inside the target areas 4 times out of 6, and within 1% on all regions. I expect next year will be less predictable and so am instead going to focus on the high-level metrics in order that we can try to get some kind of baseline and hopefully draw some confidence in investing going forwards.

I have spent a great deal of time this year (and do on an ongoing basis) studying the situation around the availability of credit. Many make the mistake of assuming that we should draw lessons from 2008-2010 and immediately apply them to this business cycle, or to the next recession – I am totally against that. The primary fact here is that banks are 3 times as well capitalised as they were in 2008 and are so much more robust. Hence, credit availability is unlikely to dry up – banks want to lend, shareholders want returns, and property remains one of the most secure asset classes (hence why it attracts such cheap financing).

Alongside that, perversely, the current grim economic outlook for the UK (relative to the rest of the EU, and the USA, and the rest of the world) means that the price of the 5-year bonds (the price upon which the 5-year mortgage rates are set) remains very low. There is a lack of confidence in the UK economic performance over the short and medium term. Whatever your position on Brexit, it is widely accepted that the short-term impact will be impaired economic performance, and this is keeping our mortgage rates down (tick in the box!).

Immigration statistics are worth looking at for the past couple of years, because some investors rely on housing economic migrants in shorter-term accommodation like HMOs, and there are what sound to me like some unenforceable and bonkers plans coming out of the home office as we speak which are bound to have some impact on this niche in the market. Things have already changed significantly since the referendum – some because of a level of hostility, some because of a weaker economic performance and a cheaper pound versus the Euro. Let’s not forget that the housing crisis is largely caused by population growth (most of which is not organic, it is imported), alongside cultural shifts. If we had negative migration (some have mentioned it in Brexit stress-test scenarios) this ‘ever-present’ in our market would go away and cause a potential step change. This is unlikely to play out in 2019, and also the increased populism and hostility to immigrants in central Europe will also potentially play a part in making the UK a more attractive destination again. However, the conclusion must be that any strategy reliant on immigrants is a risky one in these uncertain times.

Demand is likely to continue to increase (immigration notwithstanding) as society moves more away from the nuclear family and more towards staying single for longer but wanting own space (in urban areas). Confidence in the stock market and resale prices is likely to impact the number of housing starts downwards – these are challenging times for housebuilders. Housing prices already seem to be brutally ‘optimised’ and there seems little scope for squeezing more value out of potential purchasers. The end of Help to Buy will also have impacted 5-year and 10-year plans for housebuilders. One thing I do expect to play out in 2019 is a continued flat market in the south and London and then many of the first Help to Buy loans to come to the realisation that once the new build premium has been added, and the market has gone up and down over that 5 years, that many are left in or near negative equity, particularly when thinking about the cost of moving and the stamp duty on the next potential property. This false leg-up onto the ladder will likely see people stuck in their first homes for longer (arguably, still far better than being stuck in rental) and transaction volumes are likely to stay low.

So, it is difficult to see much good news for the market – however, because outlooks are already relatively grim – and a tough trading environment sees the introduction of mandatory Client Money Protection (CMP) insurance for letting agents in England, alongside the tenant fee ban in England and Wales, the only bright side from the industry perspective is that there is not much further to fall. Rather than being a flippant comment, this seems a fair conclusion, inasmuch as a crash is unlikely but a continued slowdown and a tough trading environment is extremely likely to persist.

With the investor hat on, I would expect strategies involving resale to owner-occupiers to be very challenging and buying and holding to be a vastly superior strategy (if it can be executed correctly!) for 2019. For any flips, I will be wanting an extra 5% margin at least, and as they are already very challenging to find, that means I will likely not be doing any in 2019! Refinancing existing stock and reviewing portfolio, alongside optimising rents, is an absolute must. Don’t sell in this market unless you absolutely have to. Good luck…”

Adam Lawrence – Director at Garrison Property Services Ltd and Group Owner of Partners in Property

Editor at Letting Agent Today and Estate Agent Today, Graham Norwood

“Buy-to-let is clearly more challenging now than at any time during its history – but that in itself is not a reason for avoiding it.

“Buy-to-let is clearly more challenging now than at any time during its history – but that in itself is not a reason for avoiding it.

It sounds like a cliché but that doesn’t mean it isn’t true – choose locations where jobs and transport are still strong, go for secondary locations where capital values are reasonable and so rental yields will be good; and make the investment for 10 or 15 years so you have a chance of reasonable capital appreciation.

Furnish, equip and maintain your buy-to-lets well, and ensure it’s managed by a strong letting agent, because Build To Rent is coming to a location near you soon, and you need to compete with it.”

Graham Norwood @PropertyJourn – Editor at Letting Agent Today and Estate Agent Today

Founder at The Property Voice, Richard W J Brown

“Last year I spoke about the uncertainty that surrounds Brexit having a potential drag on the residential housing market. It feels like Groundhog Day as Brexit uncertainty remains, perhaps even more so! The upshot of this is that many people have been sitting on the sidelines waiting to see what happens, which has slowed down transaction volumes. That said, there will always be people that need to move for whatever reason, so there will be some transactions, just not as many as we need to have a vibrant housing market. However, the lower transaction level has helped to keep prices stable, especially in London and the south-east, which may have dipped further if more people had to move.

“Last year I spoke about the uncertainty that surrounds Brexit having a potential drag on the residential housing market. It feels like Groundhog Day as Brexit uncertainty remains, perhaps even more so! The upshot of this is that many people have been sitting on the sidelines waiting to see what happens, which has slowed down transaction volumes. That said, there will always be people that need to move for whatever reason, so there will be some transactions, just not as many as we need to have a vibrant housing market. However, the lower transaction level has helped to keep prices stable, especially in London and the south-east, which may have dipped further if more people had to move.

From an investor point of view, Section 24 will continue to take a bite out of rental profits as the tax reduction phasing continues. Equally, additional legislation, such as the removal of the three storey criteria for larger HMOs continues to send ripples through the sector. Defensive strategies, such as company BTL purchases will continue to grow, just as they have done this year already. However, whilst the headline mortgage market seems healthy enough, this is perhaps misleading when considering how may loans are for remortgage rather than new loans. This all suggests a fairly stagnant BTL sector for the immediate future, which may slip into the red with a cliff-edge no-deal Brexit causing a lack of confidence generally.

Brexit aside, the increased professionalisation of the PRS will continue, with larger landlords and build-to-rent players dominating the growth in the sector for new rental properties. Accidental landlords will probably look to exit if their cash flow turns negative and the sector will probably continue to split into a two-speed market, with smaller ‘BTL is my pension’ investors remaining, along with the larger & professional landlords, but with some of the middle-classes potentially seeking simpler, more tax-efficient investment returns elsewhere. So, overall, I see a sluggish market with some consolidation and segmentation, as the uncertainty, continual change and cloudy political-economic situation remaining. As always though, there are opportunities for the astute or entrepreneurial investor that can adapt to the climate to capitalise, which is where I aim to be myself.”

Richard W J Brown a.k.a The Property Voice @PropertyVoiceUK | Listen to the podcast here

PropTech Influencer and Global Speaker, James Dearsley

“The property market is starting to understand that it is going through a period of intense change. The traditional view that we are a relationship-driven marketplace is beginning to warp into the view that we are becoming a tech-enabled industry and one that is on the start of a process known as digital transformation. As a consequence, we have seen an almost ubiquitous use of the term PropTech in the past few years which is the symptom of this change.

“The property market is starting to understand that it is going through a period of intense change. The traditional view that we are a relationship-driven marketplace is beginning to warp into the view that we are becoming a tech-enabled industry and one that is on the start of a process known as digital transformation. As a consequence, we have seen an almost ubiquitous use of the term PropTech in the past few years which is the symptom of this change.

In 2019, I expect to see the real estate industry struggle with this new industry as it looks for ways to become more streamlined, efficient and customer focussed whilst trying to retain its traditional format. We have seen huge case studies of failure of so-called PropTech businesses, many of whom featured in last years predictions for 2018 in fact, but this should dissuade traditional businesses from understanding the changes being demanded by the consumer. We are all looking for better processes, improved systems, more cost-effective workflows and ultimately to see an industry transition to one that works for everyone.

There will be more failures in 2019 as the 6,000+ PropTech businesses around the world continue to find their place in an industry that is rigid and slow moving but there will be many more successes as businesses start to understand different business models, and start to evolve. One key element of this is for the industry to be welcoming of new models, work with them to understand what they are trying to do differently and come to a happy medium that means both work. Collaboration and consolidation will be a key outcome in 2019 and some will end the year key winners as digital transformation takes hold.”

James Dearsley @JamesDearsley – PropTech Influence, Global Speaker and Co-Founder of Unissu, a global PropTech search portal

Managing Director at Dataloft, Sandra Jones

“2019 may be the year in which Brexit gets decided one way or another, when work on Crossrail is completed and Kit Malthouse celebrates a full year as Minister for Housing.

“2019 may be the year in which Brexit gets decided one way or another, when work on Crossrail is completed and Kit Malthouse celebrates a full year as Minister for Housing.

Or it may not – because, as 2018 has shown, predictions are dangerously unreliable.

There seems to be a broad consensus about what will happen to house prices and transaction volumes next year – very little and very low.

But it will vary from place to place depending on local circumstances and there are a surprising number of trends that could influence local conditions, despite the lacklustre outlook overall. Here are ten to watch – factors that will drive outperformance in some areas in 2019.

- Pro-active local public landowners. The government has set ambitious housebuilding targets, private sector housing delivery is slowing and public sector bodies need new sources of revenue after years of austerity. Look out for areas with pro-active public sector bodies working with the private sector to unlock opportunities.

- Infrastructure. New transport connections are well-known to boost house prices. London has a new Cycling and Walking Commissioner, Will Norman, and following mixed reactions to cycle super-highways, they are renamed as the more user-friendly ‘Cycleways’. Worth checking out the routes.

- Personal transport. E-scooters are set to be a popular Christmas present this year. Regulation around pavement/road sharing is not resolved but they offer a low cost and rapid way to get around the city and will influence perceptions of distance and accessibility from home to work or leisure activities.

- Build to Rent. The purpose-built rental sector continues to gain momentum in a wider market. Rather than focussing exclusively on well-paid young professionals in London, investors are now looking at the mainstream and family markets in core cities and beyond. It will compete with existing PRS by offering a branded and highly professionalised management service and is there to pick up the slack if small investors lose heart.

- Working from home. It’s hardly a new concept but homeworking is finally becoming an established and accepted part of the normal working week – but it’s most likely to be a mix of workplace, home and other spaces. Developments with facilities for homeworkers will appeal to agile workers. Alternatively look for mature coffee shop culture or provision of co-worker space around stations and on high streets.

- Cities with brains. The concept of a ‘city brain’ with a web of sensors gathering data and feeding into a vast analytical infrastructure is becoming operational as technology catches up with the smart city vision. Alibaba has projects in several Chinese cities and Google has an experimental in Toronto. The UK identified AI and data as one of four ‘Grand Challenges’ in the Industrial Strategy. Keep an eye on cities at the forefront of the city brain evolution in the UK.

- Living on the high street. Permitted Development Rights – the automatic right to convert office space to residential – created tens of thousands of new homes and now retail space is up for grabs too. Given the parlous state of the retail market, this seems likely to spawn a new generation of homes on the high street.

- Connectivity. Broadband has become a key decision criteria for home-buyers and renters. As one of our blogs recently put it: To those who use it for work, connectivity is not a consumer choice, but a factor of production. Worth reviewing the providers to see where they plan to improve connectivity speed or coverage next.

- Online or high street agents. Fewer people are now forecasting the demise of the traditional high street agent but consolidation still looks to be on the cards. Another tough year with low transaction volumes will create a competitive marketplace and put the spotlight on costs and service levels. We are likely to see some losses, some mergers and the most professional rising above the rest – adopting tech…

- PropTech. Like all tech sectors, PropTech has its success stories and its failures but there is no doubt that tech which helps the industry to deliver a better service at a lower cost will gain traction. More efficient property management, facilitating community engagement, matching demand with supply and market intelligence will all benefit users and providers. Savvy budgets will focus on business solutions rather than flashy technology. Platform and integrations will bring together the strongest offers.

And in case that wasn’t a long enough list, I took a look at the results from a futures scanning bot. It threw up two big trends for 2019 that I hadn’t considered: Human Augmentation and Transhumanism. Food for thought?”

Sandra Jones @DataLoftUK @SandraRamidus – Managing Director, Dataloft

Chairman at Acadata, Peter Williams

“Writing last year we forecast slowing house price growth and rising uncertainty and both have been delivered!

“Writing last year we forecast slowing house price growth and rising uncertainty and both have been delivered!

Indeed based upon the Acadata index we now have falling real house prices alongside small nominal gains. Acadata does not produce a formal forecast and indeed this year it is possible others who regularly produce such metrics will choose not to do so given the extreme uncertainty that now exists with respect to 2019.

It is hard to see anything other than a continuing slow down in the market for both 2019 and perhaps a flattening in 2020. There will always be those who have to move alongside others that chose to move, given their personal circumstances and preferences. We would expect transactions to remain roughly the same.

The Bank of England has rightly set out possible housing market effects flowing from different Brexit related outcomes and their impact on the macro-economy. Clearly they were hugely assumption driven and no one was suggesting that is what will happen. The events surrounding this first half of December have added to the scale of uncertainty for both the market as a whole and individuals.

For the most part the UK housing market is a domestic market driven by UK consumers and providers. In a slowing or static market we will have intensified competition for mortgage lending. The mortgage market is dominated by 4 main lenders (some 70% of supply) while around 120 lenders competing intensely for 10/15% of the market. This should ensure borrowers are well provided for.