In an age where technological capabilities are accelerating at an unprecedented pace, it’s often striking how conveyancing still remains in the dark ages.

Much comes down to the fragmented and overly bureaucratic processes that govern buying and selling properties. We have one of the oldest land and property registers in the world, and simply expecting a seamless analogue to digital transition wouldn’t be realistic.

Yet, in spite of the challenges, the HM Land Registry has been making notable inroads into developing a more cohesive digital platform. Over the last couple of years, the institution has been collaborating with Conveyancing Association and the Council of Licensed Conveyancers to explore how land registration can be executed more efficiently and cost-effectively.

We were fortunate enough to speak with Lauren Tombs, Senior Product Manager to find out more…

RS: Could you tell us a little bit about your role at the Land Registry?

LT: I’m a Senior Product Manager at the Land Registry and I work within our Digital, Data and Technology directorate. For the last year and a half, I’ve been principally involved with Digital Street – the Land Registry’s research and development project. My role is to own the vision and focus on what services we could develop in the future, taking into consideration both user and wider business needs.

What is Land Registry’s Digital Street?

RS: Perhaps we can start with the basics… Could you provide us with some information of what Digital Street is?

LT: Land Registry wants to be the world’s leading land registry for speed, simplicity and an open approach to data.

Digital Street has been an opportunity for us to explore how the Land Registry and the wider conveyancing process could work in the future – as outlined as part of our 5-year Business Strategy that was launched in November 2017. Our aim has always been to collaborate with the industry and throughout 2017 we engaged with various stakeholders across the home buying and selling process. Our aim was to understand the pain points and look for opportunities to embrace innovative technologies that are positively disrupting the industry.

We see Digital Street as an ‘enabler’ for the Land Registry’s business strategy over the coming years. Now, perhaps more than ever before, it has become fundamental to keep up with the industry’s movements and not get left behind.

Note that Digital Street wasn’t launched as a real service like others such as a Sign Your Mortgage Deed (see below).

RS: Can you give us an idea of the types of stakeholders you collaborated with?

LT: We engaged with over 50 organisations working in the property industry. For us, it was a good opportunity to hear different insights from conveyancers, lenders and estate agents all the way through to software providers and start-ups in the PropTech / FinTech space.

RS: What have been the main observations/concerns you have with conveyancing process as it currently stands?

LT: One of the constraints is the lack of transparency in the process. There is also a lot of duplication and essential property data could be made more accessible earlier on in the process, especially around the property’s title. Making informed decisions on this basis remains a challenge.

The duplication of ID verification was another one. There was a general feeling that there should be a better way of checking ID – which is completely understandable considering there are so many parties involved in a property transaction.

Our focus was to then explore how we could solve these key problems with the property industry. The difficulty is moving towards an end to end digital process. It’s never going to happen overnight – changing the buying and selling process to where we need it to be will take a long time.

RS: Sure, I can imagine that things are always evolving and what might be the case today may change. It’s almost unpredictable in a lot of ways…

LT: Yes, absolutely – we’re looking at emerging technologies and learning as much as we can at this moment in time. However, things could change quite dramatically over the next five years, and I think they will to be honest.

Sign Your Mortgage Deed Service

RS: Could you discuss the progress achieved thus far with the rollout of the Land Registry’s ‘Sign your Mortgage Deed’ service?

LT: This service is currently ‘in-flight’ and is part of Land Registry’s wider Digital Programme which is aimed at building better services for our users and opening-up more of our data.

The first digital mortgage was registered in April 2018 and we’re continuing to collaborate with our launch partners – Coventry Building Society and Enact. The plan is to gradually start rolling out this service across England and Wales.

RS: Good to hear things are progressing in the right way. Are the efficiencies measurable or is it too early to deduce what is happening?

LT: It probably is too early to comment. We are focusing on remortgages only for the time being and already seeing how the service could be scaled up to actual mortgages and property transfers

Although Digital Street is not a service like ‘Sign your Mortgage Deed’, it’s having a significant influence on our future work. Moreover, we’ve got the industry talking which is one of the key things that we want to achieve with Digital Street. It’s important that as an industry we explore this problem together.

Blockchain and Smart Contracts in the Property Industry

RS: What other research and development projects are coming out of the work at Digital Street that you could tell us about?

LT: Following our engagement with the property industry, we created three proofs of concept to demonstrate the sorts of services that could be developed in the future – all based on the assumption that we had better access to property data, a more intelligent Land Register and made use of emerging technologies.

One of them explored how smart contracts on a blockchain could work in conveyancing and land registration. The idea was to show how the exchange/completion process could work digitally and be simpler for users. It was a very basic smart contract being drawn up between a buyer and a seller – this would be digitally signed and then automatically invoke the movement of the funds for purchase and the automatic update of the Land Register.

RS: So, the idea is to digitise provenance, ownership, transferability etc. and effectively put it on to a blockchain protocol?

LT: Yes, that was the concept we developed. The land register itself was instantly updated via the smart contract and so was the payment of Stamp Duty. We get asked a lot about what our position is on blockchain and smart contracts, especially as other Land Registries across the world have started to explore and adopt this technology. Implementing this proof of concept was to prove that it could be done.

One of our main goals is to understand the intricacies of blockchain, distributed ledgers and smart contracts so we’re very keen to continue exploring the possibilities, bearing in mind that the technology will have its own application in England and Wales. For example, we’re currently looking into how it could impact the future digital land register.

RS: I’m aware that in Dubai the government has bold targets to digitally record and process all transactions using blockchain technology by 2020[1]…

LT: Yes, their Land Registry has been established for a lot less time than ours, so they can accelerate things much faster. They also already have digital identification already in place for the entire country.

Property Assistant and Digital Mortgages

RS: All very interesting. And you mentioned that there were two other concepts you were working on?

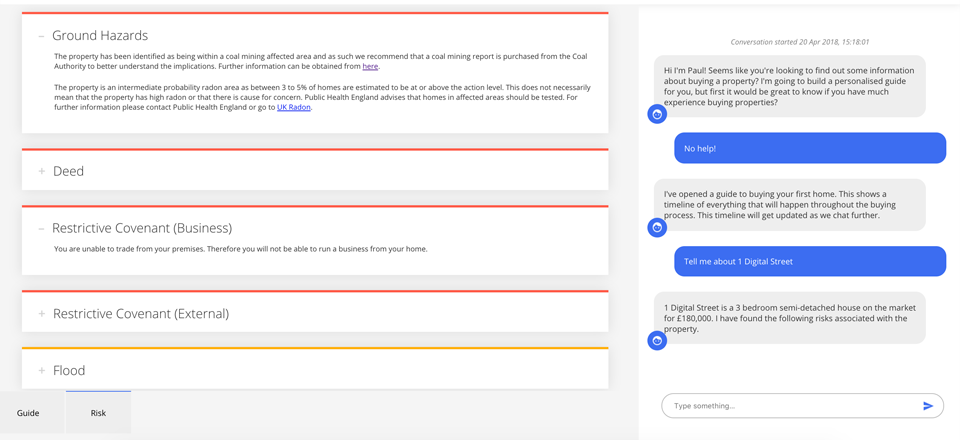

LT: Sure, we also developed the idea of having a “property assistant” – essentially front-loading key property information at the start of the process. This could help people make more informed decisions on whether to buy or not. We worked with different providers to pull in the data from a number of places, the idea is to provide access to a large property database that would operate in real time. For example, a property located in a flood risk area or on a mineshaft could be identified much earlier. Potential legal risks such as restrictive covenants and negative easements can also be viewed.

The Property Assistant enables homebuyers to access real-time answers to their questions surrounding any property in England and Wales.

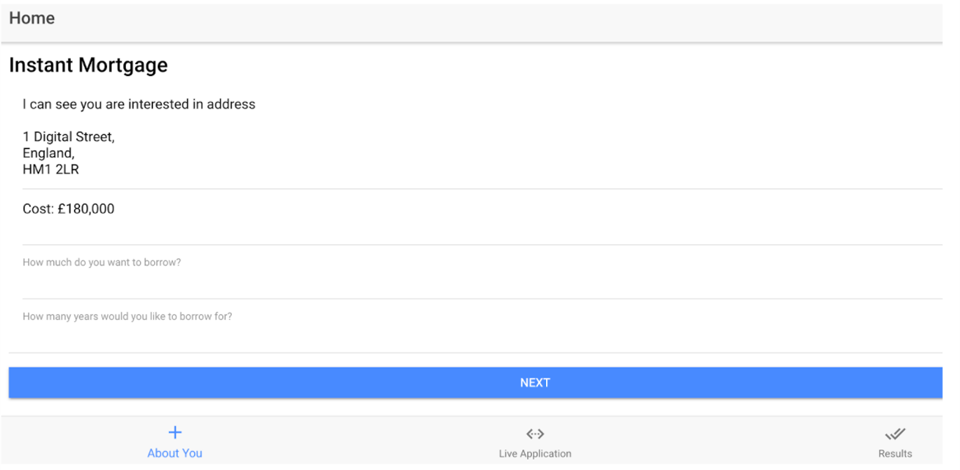

The other concept we explored was instant mortgages. This concept had all the information pertaining to the applicant including ID verification, income, deposit and other affordability assessment metrics instantaneously available alongside key data related to the property the applicant wants to purchase. Borrowers could then readily access a list of pre-approved mortgages or secured loans which could streamline the lending process.

Instant mortgages apps would look for relevant information about the buyer, check data sources for risks and present a list of pre-approved mortgage deals direct from the most suitable lenders.

RS: Yes, there are several digital mortgage brokerage firms already tapping into this space such as Habito and Trussel.

LT: Yes. It’s important to note that we’re not developing these concepts in real life ourselves, nor are we dictating how the industry should innovate and develop their own models. It was more around showing the sorts of services that could be developed if we had better access to property data, Artificial Intelligence, smart contracts etc.

RS: I would also imagine that ensuring that minimising property title fraud and other forms of hacking, cybercrime etc. is a priority as you are developing these concepts?

LT: Yes, the proofs of concepts are really about exploring the possibilities. If these sorts of services were to be developed in the future, security will be at the forefront of anything that we do.

RS: Looking at a 5, 10 and say 20-year trajectory, how much do you feel the conveyancing process will be dehumanised? Based on your research thus far, how would you envisage the role of conveyancing solicitors and other intermediaries?

LT: It’s not really our place to comment on what their roles would be. However, these industries have always learnt to evolve with the times and I would imagine they will continue to do so.

At the Land Registry, we have started to look at how we can use technology automate some of our internal processes enabling our caseworkers to focus more on the complex work, utilising their unique skill set. I think others are likely to follow a similar path – although it’s often hard to place a specific timeline.

RS: How can readers find out more about Digital Street’s ongoing work?

LT: I would keep an eye on the Land Registry’s external blog. We will be publishing our ongoing research and development work, so your readers can stay up-to-date.

[1] See this and global case studies of blockchain at work in the property industry.