Held in late June 2017, this half-day conference explored some of the issues of the day facing the student housing sector – with a range keynotes and panel discussions involving investors, agents, sector professionals, amongst other stakeholders and representatives. Topics approached included the current state of play and challenges; ongoing investment interest; an innovative student mortgage finance model; perspectives from a student landlord; how to balance quality with affordability; student housing development financing and some direct insights into how the sector is attending to real student needs.

We have outlined some of the key takeaways from these presentations over this long-form post. Please click on the links in the contents box below to head to specific topics of interest and use the arrows to scroll back up.

The State of Play and Challenges for the Student Housing Sector

- Karen Burke, Head of Accommodation Services, Sheffield Hallam University and Chair of the Association for Student Residential Accommodation outlined how there have been recently been fewer 18 year old student applications, reflected in the reported decline in this year´s UCAS application numbers (a 5% drop relative to 2016);

- There has also been a 7% drop in EU-based applications (comparing 2016 with 2017);

- There are currently 330,000 university-owned and managed beds and 540,000 purpose built student accommodation (PBSA) beds, excluding the private rented sector;

- As the second largest expense after fees, universities are placing a strong priority on safeguarding their assets and ensuring that standards are kept high which, it is hoped, will aid student retention;

- Universities are increasingly looking at partnerships as a way forward rather than exclusively investing themselves;

- Burke also raised the issue of growing rents – particularly as more students are concerned about their ability to afford decent accommodation. “Not all are able to go to the bank of mum and dad”, she highlighted;

- Word of mouth continues to play a big part in the marketing of student accommodation at all levels: Twitter, Facebook, Snapchat, Instagram can all make or break a property’s reputation by one click on a mobile phone;

- Mention was also made of the risks of studio investments. Many remain vacant as first-year students prefer a more sociable experience. Whilst “twodios” are being claimed as the “next big thing”, there are risks if, for example, one student doesn´t connect with the other he/she is sharing with;

- On this issue of examining what students actually want – developers should ask, for example, if there is genuine demand for “trendy common spaces” (with private dining, cinemas, games rooms, changeable furniture, study areas, focal points etc.). Permitted Development Rights office conversions were also mentioned as being increasingly problematic in this regard and there is a prevalence of developers moving forward with schemes despite them not being in the best interest of local student communities.

Investment Interest in the Student Housing Sector

- Although indicating that the headwinds may be growing, Jacqui Daly, Director of Residential Investment Research & Strategy at Savills gave the audience an overall positive picture for student housing;

- The delivery of purpose built student housing has helped not only the British university sector become competitive on a global scale but also the property market as a whole. Valued at approximately £20 billion, with between 70,000 to 80,000 beds traded every year, the sector has emerged as an asset class in its own right – now competing with several commercial sectors in terms of scale;

- However, reflecting on the last 20 years, she argued that the environment has changed considerably. Construction costs, for example, were considerably lower – which is having a noticeable impact on the viability of schemes, especially those in more marginal locations and cities across the UK;

- Other factors causing concern include higher tuition fees and immigration policies which, in turn, are expected to filter through to investors’ confidence in the market. On this latter issue, Daly referred to the Savills report published in early 2017 – noting that the lesser amount of overseas students coming to the UK could well have a strong effect on market dynamics particularly at the higher end of the student housing sector. With students having to pay more for their education, many are choosing to go to higher and better ranked universities – which she believed could lead to some form of “consolidation” over the coming years;

- Daly highlighted a potential oversupply risk in some markets. However, broadly speaking, the overall student-to-bed ratio remains about 3 to 1. Local markets where the ratio is falling below 2 may have some cause for concern. Interestingly, facing such scenarios, some developers are pivoting to other sectors within the residential space such as co‐living and build‐to‐rent;

- Nonetheless, Daly underlined how pension funds are actively in search of income generating investments and blended returns. Citing a Canadian Pension Fund investing on behalf of some 20 million people, the appetite to get into asset classes like the UK student housing sector remains very strong. For these kinds of investors “big is beautiful” – meaning that some of the issues around occupancy rates in some schemes can be overridden to a certain degree.

An Innovative Student Mortgage Finance Model

Dick Jenkins, Chief Executive, Bath Building Society presented an innovative student mortgage finance model first implemented in Bath prior to expanding to Sheffield, Cardiff, Aberystwyth and Norwich, amongst others. The product essentially provides a 100% mortgage finance on student let properties – securitising the equity in their parents´ property. Students typically become live-in landlords with their housemates contributing towards the mortgage.

Jenkins pointed out that overcoming the regulators doubts in pushing forward the product did, perhaps unsurprisingly, pose some difficulties. However, incorporating a collateral charge with pledged equity from the parents´ home eventually rendered the product relatively risk free from an underwriting perspective, particularly as many parents who express an interest would largely have a small or no mortgage on their principal private residence. In a repossession scenario, there would still be an above-sufficient level of equity to fire sale the property and use the proceeds of sale to clear all secured debts.

Another interesting advantage from a tax perspective is that, as the student owner is in the property for over 36 weeks, it is classed as their primary residence – meaning that Capital Gains Tax (CGT) does not crystallise at sale. Jenkins also confirmed that, in ten years of running the product, there has not been one default.

Nonetheless, Jenkins mentioned that the product is not for everybody and it can be a relatively complicated sale. The student, for example, would have to be organised and responsible. It would obviously be in the best interest of the parents to make sure that everything is being run well and, naturally, the mortgage is being paid on time.

Perspectives from a Student Landlord

Carolyn Uphill, Chairman at the National Landlords Association (NLA) provided the audience with some interesting views from her own experiences as a “hands‐on” landlord since 2003 with four HMOs in Manchester (housing a total of 19 students);

- The NLA works with over 79,000 landlords throughout the private rented sector, including many student landlords;

- She reminded the audience that the private rented sector as a whole has been “drowning” in relentless legislation and regulation in recent years. The changes to tax relief on mortgages, for example, has only just started to come into force and many NLA members believe they are being squeezed out of the market;

- With the further cost of purchase increasing by 3% due the stamp duty surcharge, the NLA´s most recent survey has shown that the overall proportion of landlords looking to expand their portfolios is at an all‐time low of just 13%;

- Rental returns on student property have to be good due to the wear and tear (which are now non-tax deductible) and maintenance costs being higher. There is more admin and many more callouts relative private residential lets;

- Most student houses have three or more unrelated tenants and are therefore subject to Houses of Multiple Occupation (HMO) management regulations. Uphill argued that extending the licensing requirement is likely to impose extra bureaucratic criteria which, in turn, will add to the existing pressures on landlords to raise rents or sell up (potentially affecting supply);

- The proposal for minimum room sizes is also likely to create problems. In Uphill´s experience, the growth of purpose built student halls has not dimmed the enthusiasm for second‐year students to live in a house with a group of their own choosing as a “rite of passage” at university. Describing such houses as real properties, she asserted that any arbitrary limit on room size will inevitably take accommodation out of the system. The licensing and prescriptive route, she also argued, is not always the best way to encourage high standards and the best landlord/tenant relations;

- Another concern relates to the Immigration Act and Uphill was particularly critical of the requirement to see and record ID documents from all prospective tenants. She highlighted how she has not had one single sign‐up session where somebody in the group hasn’t failed to turn up with the requested documents. She did mention, however, that foreign students do understand that they need ID and generally do have their passports with them;

- Uphill concluded by pointing to the fact that rents have risen steadily in recent years for these reasons and the advent of plush, private halls has raised expectations. Students have become more demanding and overall standards of fixtures and fittings have risen in response;

- Uphill also commended the work of bodies such as Manchester Student Homes and the Leeds Rental Standards that are tangibly rewarding landlords for adopting accreditation schemes and signing up to meet certain standards of accommodation. In return, landlords are given preferential promotion to the student tenant market;

- More students send automated Instagram DMs to find accommodation directly with landlords. Institutional PRS providers would be wise to think more about this communication channel.

Student Housing – Balancing Quality with Affordability

- Martin Blakey, Chief Executive at student housing charity Unipol spoke on some of sector´s the practical considerations moving forward;

- Unipol is based in Leeds with offices in Nottingham and Bradford. The company currently houses just over 3,000 students and provides accommodation ranging from small houses to larger multi-let buildings;

- The organisation also operates the ANUK/Unipol National Codes and runs a number of accreditation schemes – currently covering 274,000 bed spaces;

- Caveating that there has not been a reliable update of figures since 2006, Blakey estimated that there is approximately 23-24% of students living in purpose built accommodation, 45% in the private rented sector (“off street housing”), 10% in their own home and 22% living with family;

- Using Leeds as a point of reference (which Blakey understood to possess broadly similar characteristics to cities like Manchester Liverpool, Newcastle and Nottingham), virtually all first‐year students are going into halls. 64% of returning students (after the first year) live in off-street housing. The 11% of returning students living in purpose built student accommodation in 2012 had increased to 13% four years later, which is pretty marginal when considering the growth of this particular form of housing in Leeds over that period;

- From a national perspective, unless a developer is working in a winning university town or there is a noticeable accommodation shortage then demand for student housing tends to be static;

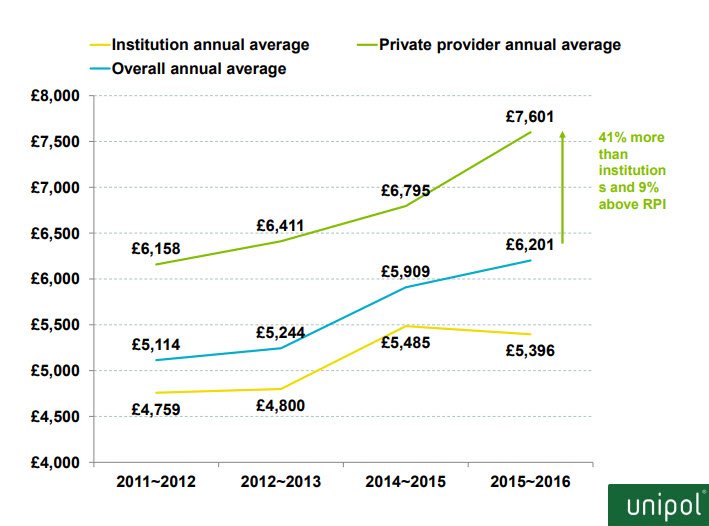

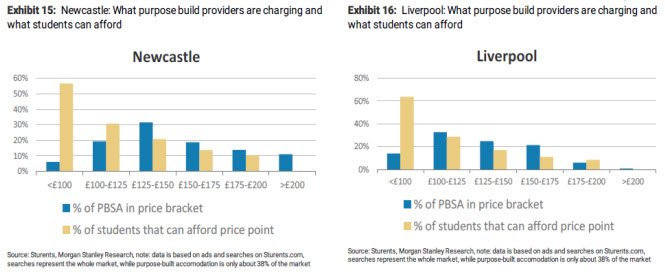

- The private sector has made significant strides in student accommodation provision (from 18% in 2006-07 to 41% in 2015-16) – however several questions remain surrounding affordability. Blakey believes that private developers are being driven by hopes of higher yields that satisfy investors and not students´ The first graph below, for example, demonstrates the visible difference between rents for private student accommodation relative to university-provided housing and the overall annual average. The two charts underneath also demonstrate that students in cities like Newcastle and Liverpool are only realistically able to afford sub-£100 units – yet the supply of this type of stock is clearly insufficient:

- Blakey also pointed to the growth of consented student accommodation schemes in areas with static or declining student demand (London, Manchester, Liverpool, Cambridge and Southampton were all cited as having a significant number of empty rooms). He believed that serious surpluses could arise in the coming years.

Financing Student Development Projects

- James Woolley, Partner at the Knight Frank´s Student Property Team spoke on the organisation´s work with some of the major funds operating in the student housing sector – including the likes of Black Rock, GCP, Lothbury and Aviva;

- Knight Frank valued over £7 billion worth of stock in 2016 (ranging from the premium products to first-generation accommodation both in the UK and increasingly in Europe);

- On the agency side, Knight Frank has also acted on some of the key transactions in recent years – including the Aston student village (the largest single asset transaction to date, comprising of 3,000 beds on the university campus);

- In terms of outlook, build costs are one of the most obvious concerns and are likely to go in one direction – £60,000 as a cost per bed is common which rises to anything between £70,000 and £80,000 in London, particularly when introducing a tower into the scheme;

- Woolley underlined how once a developer bolts on appraisal, profit, finance, planning costs amongst others (which can have huge variabilities) it can be hard to see a scheme stack up that does not achieve an average rent throughout the building of approximately £150 a week. The 2016 Knight Frank Index, however, demonstrated that average rents for en-suites tended to be around the £120-125 mark per week. With studios achieving between £150-160, it is understandable why developers are keen to push these models forward to investors despite the lack of genuine demand;

- Another observed issue is land owners’ over-estimation of the worth of their sites which has become another barrier to development;

- Woolley believes that the sector needs to evolve and move away from premium products. There is a need to provide a more affordable product for students on lower incomes that still provides good facilities and amenities;

- Knight Frank´s research on development pipelines reported that approximately 80% of projects underway are being executed by the private sector. Woolley believes this should change by means of more strategic partnerships with universities. In such scenarios, developers and owners would ideally need a 10 to 15-year agreement in place so that they can actually realise some sort of upside from the compressed yields resulting from lower rents;

- In addition to these collaborations, with build costs likely to continue to rise, more innovative approaches are also required to ultimately solve the affordability issue.

Attending to Real Student Needs (…not Just Investors)

- Einita Sohal, University Partnerships Manager at Unite Students presented some of the main findings from a 2016 report which surveyed 6,504 students;

- The research found that students predominantly are in search of community and a sense of belonging – which was deemed as far more important than what the rooms look like;

- As a result, Unite Students have enlisted welfare leads in all the cities in which they operate. These people are trained to listen to anything going wrong in student flats;

- Describing housekeeping and maintenance teams as “the backbone of our company”, Sohal also highlighted how all members of staff participate in making student good experience;

- Services managers are recruited to work directly with universities and student communities to understand the key issues. Added to this is peer to peer support – Unite has just committed to recruiting 100 student ambassadors across seven cities to guide, orientate and promote recreational activities;

- Sohal also commented how students are increasingly engaging with local communities, working with councils to build solid relationships. She cited a converted church development in Sheffield – where the university were invited to provide their thoughts on what the outcome should be. The thoughts and ideas eventually shaped what is now a hub space that is being promoted with the council as a “true partnership”.