Estates Gazette´s early May event sought to address a number present-day questions relating to the current state of London´s residential property sector.

Introduction

Against a backdrop of Sterling´s post-Brexit devaluation, a marked decline in high-end property prices and the threat of skills shortages, many of the discussions were nonetheless refreshingly directed towards sustainable, non-speculative industry growth. With the government´s housing white paper now in play, the issue of whether “action will follow talk” was deliberated alongside frequent mention of the build to rent sector´s role in tackling the Capital´s housing shortage. Other conversations included panel discussions amongst Outer London Borough council on the future of housing delivery, advancing social housing delivery in the capital´s estate communities and a very interesting debate amongst leading Housing Associations.

London´s Housing Plan

Reflecting on the first anniversary of Sadiq Khan’s mayoralty, Deputy Mayor for Housing and Residential Development James Murray‘s short presentation broadly summarised the Greater London Authority´s focus on making its housing market more equitable. As a result of £350 million of public funding, the GLA is building strong coalitions with councils to facilitate scaled delivery whilst actively encouraging the expansion of housing associations´ building capacity.

The draft Supplementary Planning Guidance (SPG) was produced on the back of conversations over summer 2016 with the various industry stakeholders. This was followed by the housing white paper which set precedent for the Draft Local Plan which should be released in the latter part of 2017. The crux of this document will be focused on pushing forward a sustainable housing strategy in line with London’s real needs. Tackling rough sleeping and facilitating the sustainable growth of a wider range tenures, such as the institutional Private Rented Sector (iPRS), were two of the expected highlights. According to Murray, the underlying goal of the Plan is to meet ambitious affordable housing targets; encourage more densification (ensuring that good design plays a crucial role in delivery these buildings); embed the requirement for affordable housing into land values and support the growth of housing that is genuinely distributed across a wide-cross section of social demographics. To quote a recent example that demonstrates such commitment, with 35% of the units being affordable, the Hub groups´ 514 home scheme in Croydon spent just 79 days from submission to consent at committee.

In the brief Q&A session, Murray acknowledged ongoing feasibility issues, a broader lack of transparency and the overhang of 260,000 unimplemented planning permissions. With the Sadiq Khan actively encouraging a “softer” Brexit outcome, the deputy mayor also expressed his concerns over EU nationals employed in London´s construction sector and the potential threat of an impending “mass exodus”.

An Overview of the London Property Market

Edward Green, senior analyst from Savills presentation started by outlining the predominant factors (for better or worse) currently shaping market dynamics, namely: the June 2017´s Snap Election, the impending Brexit negotiation process, rises in stamp duty (for both high-end and buy-to-let properties), the implications of Section 24 of the Finance Act (No. 2) 2015 on the private rented sector and, as explored briefly above, the London Mayor´s decision to prioritise affordable housing delivery. Potential interest rate rises and the rise in international demand as a response to Sterling´s devaluation may also have a negative effect.

Green also pointed to a decline in mortgaged owner-occupier purchases, principally due to affordability constraints. Even with average first-time buyer income at £64,000, deposit requirements of £89,000 are still scuppering many people´s ability to get on the ladder. Following the Mortgage Market Review in 2014, the standard mortgage income multiplier of 4x will remain for the foreseeable future – meaning that transaction levels are likely to slow down (having already dropped by 12.5% since 2016).

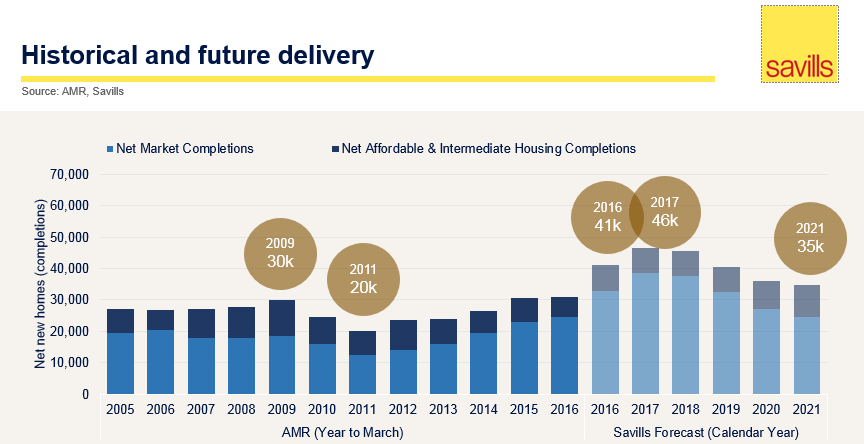

In terms of London housing supply, according to Green, the annual target of 42,000 units by the Greater London Authority (GLA) is underestimated and should be in the region of 64,000 – well over double the number of units being delivered at the peak of the global financial crash in 2009. Actual delivery is expected to peak at 46,000 units in 2017 before tailing off over the next few years to an estimated 35,000 units in 2021.

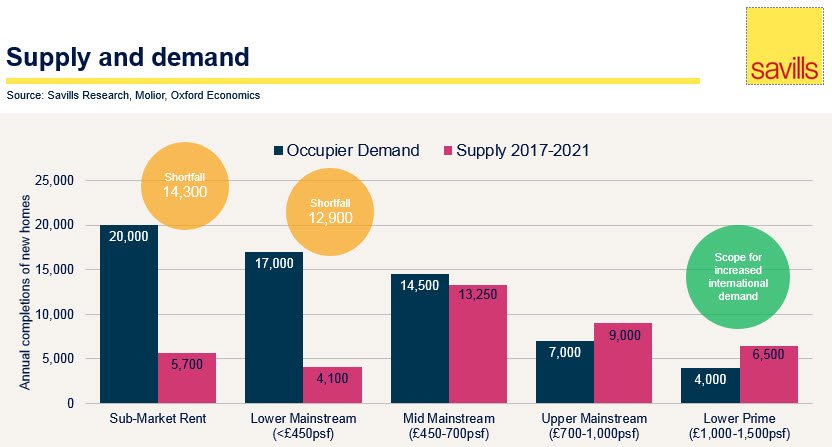

Other data pointed to the significant shortfall of London homes at lower price points, particularly for the sub-market rent and lower mainstream market segments (under £450 per square foot). The demand and supply balance for mid-mainstream units (£450-£700 per square foot) was relatively equal, yet there are clear over-supply signals of upper-mainstream (£700-£1,000 per square foot) and lower prime units (£1,000-£1,500 per square foot) – reflected in the visible correction already underway.

Construction starts and sales levels were relatively aligned until 2013. By 2015 there were 13.5 times more starts than sales. Although the gap has narrowed, there are still some 60,000 homes across the Capital that are waiting to be completed and remain unsold. This surplus, it was argued, could lead to pricing issues moving forward. Savills are predicting that mortgaged owner-occupier and domestic cash investor segments will remain broadly flat; mortgaged buy-to-let will decrease and both large scale PRS and international purchasing will rise in the coming years.

The Future of London Residential

Much of Savills´ findings correlated with a presentation later on in the morning by Nigel Evans, Head of London Residential Research from EGi. Evans´ presentation started by ordering the intensity of development initiations (from the highest number to the lowest): Tower Hamlets, Wandsworth, Greenwich, Newham, Southwark, Lambeth, Barnet, Lewsisham, Ealing, Croydon, Hackney, Brent, Hounslow, Hammersmith & Fulham, Camden, Westminster, Redbridge, Hillingdon, Sutton, Harrow, Bromley, Bexley, Islington, Haringey, the City, Barking, Kensington & Chelsea, Kingston, Merton, Waltham Forest, Havering, Enfield and Richmond.

Evans went on to highlight a 2,500-unit increase in inner London development starts and a corresponding drop of the same amount in the Outer London boroughs. According to EGi research, the pipeline of starts has remained “above water” due to these larger schemes across the inner boroughs – particularly via the construction of towers (which constitute 71% of all big schemes now in development). A small number of tower starts can have a profound effect on the overall pipeline: in 2016 there were 47 in the capital (compared to 22 in 2015, 25 in 2014, 16 in 2013 and 7 in 2012) – with notable concentrations in the Docklands, LBKD, Nine Elms, Vauxhall, Elephant & Castle and Waterloo. According to Evans, the number of tall buildings is expected to gradually spread out to new territories, with starts already underway in areas such as Wembley, Croydon and Stratford.

In terms of tower planning applications, the number peaked in 2015 at 107, followed by 75 in 2016. In 2016, 25% of all towers consented were for the Private Rented Sector (from a base of zero a few years previously) which, according to Evans, broadly represents the completion of the full circle that initiated with 1960s council house development in the form of an affordability-driven “paradigm shift away from an owner occupier dominated market to a rental dominated one.”

Projects and Opportunities Across London: Hear from the Councils

In the following panel, leading Local Authority representatives discussed their own objectives and aspirations on outer borough housing delivery.

Peter George, assistant director of regeneration and planning from the London Borough of Enfield, started by outlining how the delivery of social rented and shared equity homes is a priority. The council has set up its own development company that will take the lead on project master-planning and has secured £150 million from public sector finance for land acquisition.

Darren Rodwell, council leader from Barking and Dagenham, pointed to how the LHA is in the fortunate position of having more brownfield land than any other London Borough. In light of this, the development of social housing models will also take preference over other tenures – particularly as recent data from the Centre for London revealed that over 40% of residents are earning less than the London Living Wage. The report by the Independent Growth Commission “No-one left behind: in pursuit of growth for the benefit of everyone” has spurred plans to expand seven growth hubs in addition to establishing a development company (“Be First”) to the accelerate the delivery of 50,000 new homes. A number of riverside development schemes, the formation of the Barking Town Centre Housing Zone (with £42 million to unlock housing delivery) and various commercial and regeneration projects are all being progressed.

Patrick Hayes – assistant director of regeneration and planning from the London Borough of Ealing – whilst hailing Southall in West London as the “next Brixton”, also expressed his concern that the vast majority of London workers are still not able to afford the homes coming on to the private marketplace. Complementing infrastructure projects, the council will be focusing on scaled development models. Southall, for instance, still has a notably sized pipeline of future developments on former industrial land. The aim will be for the Local Authority to take a proactive role in site assembly and ensure that project outcomes are successful (using Compulsory Purchasing Order powers where sites are stalled and/or not being delivered). “Broadway Living”, a development company owned by the council, currently operates on a relatively smaller scale and is positioned to deliver homes for market / discounted rent, low cost / shared ownership and open market sale. Schemes through this organisation will be rolled out alongside larger project objectives such as Greystar´s predominantly build to rent developments.

Jo Negrini, Chief Executive from the London Borough of Croydon, gave an insightful presentation on the borough´s growth prospects. Described by Sadiq Khan as a “hidden gem”, Croydon is the second largest borough in London (with a population of over 379,000). 32% of the population is under 25 and the area is widely being deemed as having a significant role to play in alleviating the capital´s housing crisis (with a capacity to build 10,000 housing units in Central Croydon alone). A Westfield shopping complex, other sizeable retail and leisure schemes alongside road investment programme projects are all planned to enhance such objectives. Negrini commented on the council´s decision to implement an Article 4 Direction to mitigate the risks of office stock depletion and concerns over the quality of Permitted Development Rights (PDR) units being delivered.

Negrini also highlighted the work of Brick by Brick – a private company with Croydon council as the sole shareholder. In addition to notably sized projects such as the redevelopment of the Fairfields Halls, Negrini demonstrated a number smaller infill projects being developed on public land. Interestingly, with land being purchased at market rates from the council, developments containing 50% of affordable housing are feasible – even on smaller sites. The council will gain income through earning 100% of any development profit alongside other income generating activities. Only selling and letting units to local residents, all the value will stay within the borough. Her presentation also demonstrated how “tenure blind” design is being undertaken by architects who have a clear grasp on the local area is resulting in more cohesive project outcomes.

In the ensuing panel discussion, one of the frustrations highlighted was the “non-developing developer” phenomenon (i.e. companies holding onto consented sites and not building out). At the same time, appreciating that Outer London developers are still struggling to make things “stack up”, questions related to project viability and the rebasing of land values were raised. Patrick Hayes from the London Borough of Ealing mentioned his council´s keenness to work with developers to overcome these challenges whilst avoiding the risk of entering into non-productive affordable housing negotiations. One solution being proposed on certain schemes is to concede to more high-end units in return for planning permissions conditioned upon the delivery of more affordable homes.

Other issues discussed included the Green Belt and whether the drive for looser policy making could breed unintended consequences such as urban sprawl. Although opinions across the broader sector are divided, the panel agreed that there is a sufficient amount of of latent brownfield sites across London at the current time.

The topic of Neighbourhood Planning was also raised as a potential obstacle. Hayes pointed out that many local objections that started out embroiled in hostility usually end up positively providing there are good lines of communication in place and all perspectives are heard. He also called for the involvement of more young people and the need to move away from “Church hall” discussions that are not representative of communities at large.

London Estate Regeneration: Opportunities and Challenges

The next panel saw Kate Ives, development director at Wates Residential; Jonathan Seager, executive director of policy at London First; Simon Vevers, regeneration and strategic partnership director at The Hyde Group and Stuart Woolgar, security director at Global Guardians explore an often forgotten segment of the market. Arguably deprioritised due to the lack of project feasibility and attractiveness, the sustainable development and management of London´s estates has become of paramount importance – particularly considering that many residents have long been key drivers of the city´s economic growth. However, whilst some estates can be characterised by tight-knit and healthy communities, somewhat moving away from the “sink” label, others are ageing considerably with uneconomically high repair costs for councils to cope with. At the same time, given the well-recognised affordability constraints across the Capital, the demand for housing within London´s estates is likely to grow.

Nonetheless, on the back of the Mayor´s late 2016 “Best Practice” guide for estate generation, a number of projects are underway. In January of this year, plans were approved by Hackney Council for 400 homes on the two-hectare Nightingale Estate in Clapton (comprising of a mix of social rent, shared ownership and outright sale). These units will join more than 300 affordable homes already built by the housing association Southern Housing Trust, and nearly 400 more refurbished council homes. Hackney will be the first borough to see homes built within London Living Rent parameters (where rents will be based on a third of average local earnings).

Acknowledging the need to engender better conversations with local communities, the panel observed that the number of estate residents vehemently opposed to estate regeneration programmes is an ongoing concern. This has been more recently exemplified in Newham (east London), where a regeneration project will be going ahead despite stiff opposition from the local neighbourhood forum. Whilst the council announced that there would be “no net loss” of social rented homes on the new development, the resistance to change has been palpable and emotions continue to run high.

In such situations, the idea of arriving on an estate and simply announcing regeneration or arbitrarily imposing Compulsory Purchase Orders is a dangerous one. Despite the difficulty in coming to a consensus with existing residents, many of the issues can be overcome with engaged, albeit difficult, conversations via regular meetings, social media and other communication channels. Striking deals will ultimately require tangible and convincing change. With an overall regeneration budget of £25 million and a new company set up by the council, Homes for Lambeth is an interesting example of progress. During the project´s initial stages, residents were invited to interview development consultants and collaborate on the future direction of their local community.

Admitting that developers in the space tend to overly focus on the bottom line, Kate Ives highlighted the growth of “triple bottom line” investing which will require more of a patient capital strategy. Estate regeneration projects can last between 10 and 20 years and are prone to the whims of market cyclicality, changing faces of neighbourhoods and other extraneous factors. These projects require flexibility and nimbleness – particularly during the decanting process where community cohesion is at its most vulnerable. Other strategies include bringing a wider range of tenures and housing offers – from PRS and care housing to community, sports and educational facilities under the aim of removing the “segregating” effect that still, by and large, characterises the wider perception of London´s estates. Achieving this goal is also likely to attract a wider range of stakeholders and investors.

Why We Should Care About Housing Associations

The penultimate panel discussion of the morning involved Jules Bickers, director of housing at Capital Real Estate and Infrastructure; Kate Davies, chief executive at Notting Hill Housing; Pete Gladwell, head of public sector partnerships at Legal & General Investment Management; Killian Hurley, chief executive at Mount Anvil and David Montague, group chief executive at L&Q.

The importance of these social enterprise-based models was underlined as having a fundamental role in bridging the gap between the private and public sector and, ultimately, alleviating London´s housing shortage. Largely funded by taxpayers, the “dividends” are paid back in the necessary, albeit intangible, form of sustainable community development. While PLCs and financial institutions remain reluctant to be involved in the sector, the consensus among the panel was that, to achieve scale, housing associations need to move beyond just being grant recipients (L&Q was cited as a primary example of an organisation stepping up to the plate). As with the regeneration of London´s estates, discussed above, a patient capital investment strategy is more aligned with the core placemaking and community development objectives that should underlie any housing association development scheme.

Embracing the model of incorporating full market sale value properties into business models, more housing associations are using proceeds of sale to reinvest into further socially-focused housing projects. With this latter strategy, however, care needs to be taken to not get caught up in the vagaries of London´s speculative property market. Tenants must also be treated fairly, especially when it comes to the question of affordable rents, service charges and community integration (mixing high and low value housing may create a number of complex issues, for example). Mention was also made about the Conservative government´s extension of the Right to Buy scheme to housing association tenants in terms of the need to ensure that there is full accountability and all capital receipts are spent efficiently.

Concerns included the Brexit-fuelled skills flight, rising import costs, falling quality standards and the inefficiency of the fixed-price contract model were all discussed. Future challenges will ultimately require housing associations to be adaptable to change and, crucially, embrace a long-term perspective built on sustainable property development models.

How Can Developers Use The Government Shift in Focus to De-Risk Through the PRS?

The final panel of the morning with Andy Barnard, partner at Trowers & Hamlins; Ray Rafiq-Omar, managing director at Unmortgage; Andrew Saunderson, director of investments at Grainger and Hayley Scott, relationship manager at Investec Bank. The discussion started by noting the huge leaps made by the sector in recent years which, predominantly owed to the lack of affordability and the more transient nature of the younger workforce, looks set to continue.

The modern tenure has been supported by a “wall” of institutional funding and ever-firmer commitment to invest in larger schemes. The perception thus far is that lenders are currently favouring the asset class as they are largely dealing with one purchaser (“the landlord”) for a single building. There are scaled efficiencies to be taken advantage of, mitigated absorption risks and an ability to more confidently forward-fund deals. The London build to sell sector, in contrast, has become increasingly characterised by cost overruns amongst other systemic and market-led risks. It was commented that common issues such as high development costs and skills shortages are somewhat attenuated as a result of BTR being a long-term investment strategy.

Rayhan Omar, however, disagreed with the other panellists – asserting that the inherent British aspiration of owning one´s own home is being suppressed. He also criticised the inadequate size of many PRS units being delivered. Buildings are being “calculated and not designed”, he argued, and many developers may not fully aware cost-intensiveness of the model from a running yield perspective, which may displease institutional investors in due course.

Other members of the panel, admitting the untested nature of the sector, rebutted by affirming that the growth of build to rent represents a changing market psychology. It was claimed that renting as one gets older is not as stigmatised as before and can be a decision made at a particular point in life that does not necessarily preclude people from eventual homeownership. In terms of quality, it was argued that standards are improving and, as more BTR developers move towards purpose-built models, many will be forced to cater specifically to the needs of customers, moving away from a “one size fits all approach” – or risk simply being pushed out of the market. Sigma Capital were also cited as an example of a developer delivering high quality housing (the company recently launched a £250m PRS vehicle with an initial investment of 9.99% from the Homes and Communities Agency).

It was nonetheless commented that PRS developments are not suitable in certain areas and shared homeownership, rent-to-own and other mixed-tenure schemes may be more appropriate. Depending on location, therefore, “middle ground” PRS models will be necessary to secure project viability as the sector evolves and develops its own specific nuances.