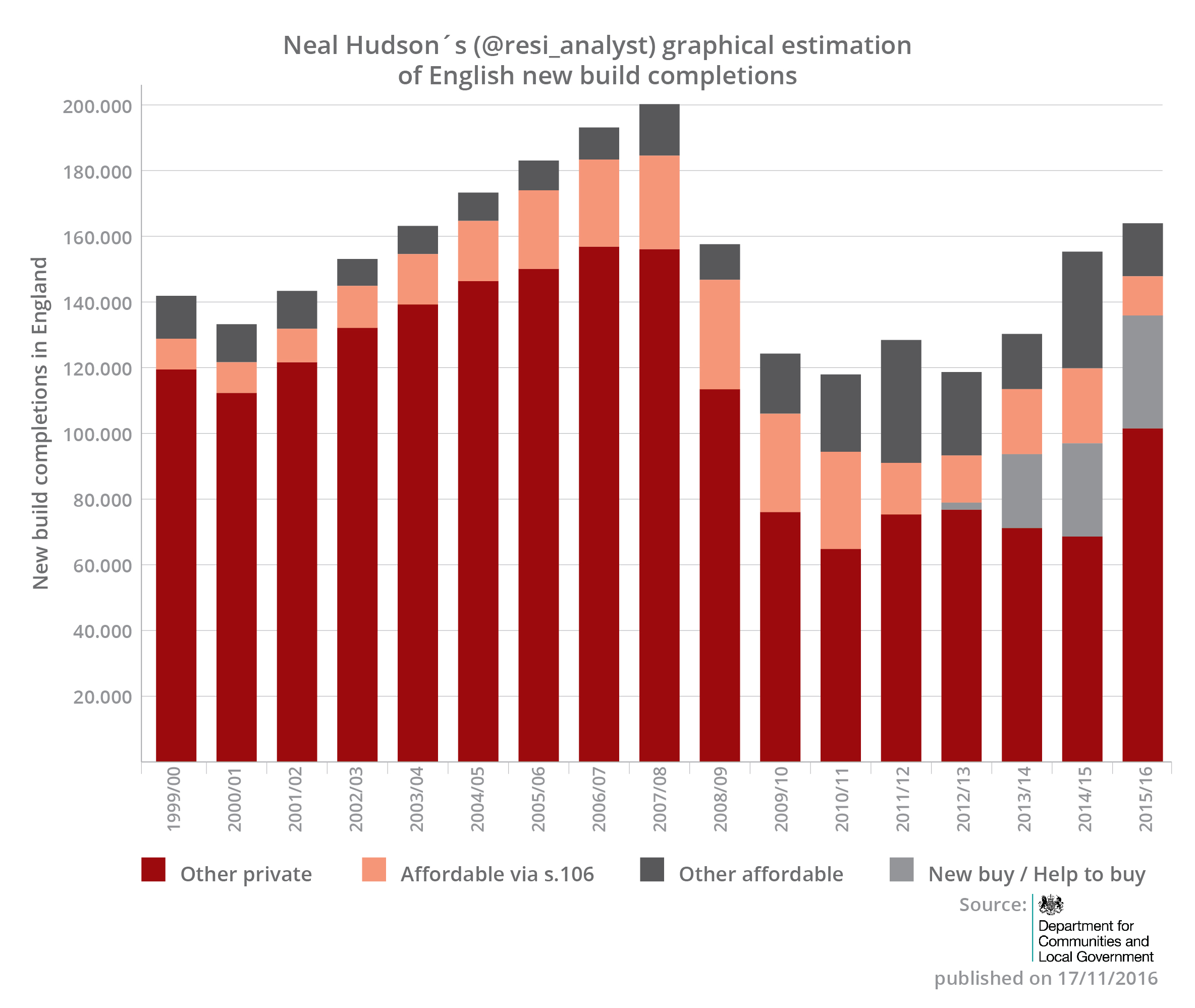

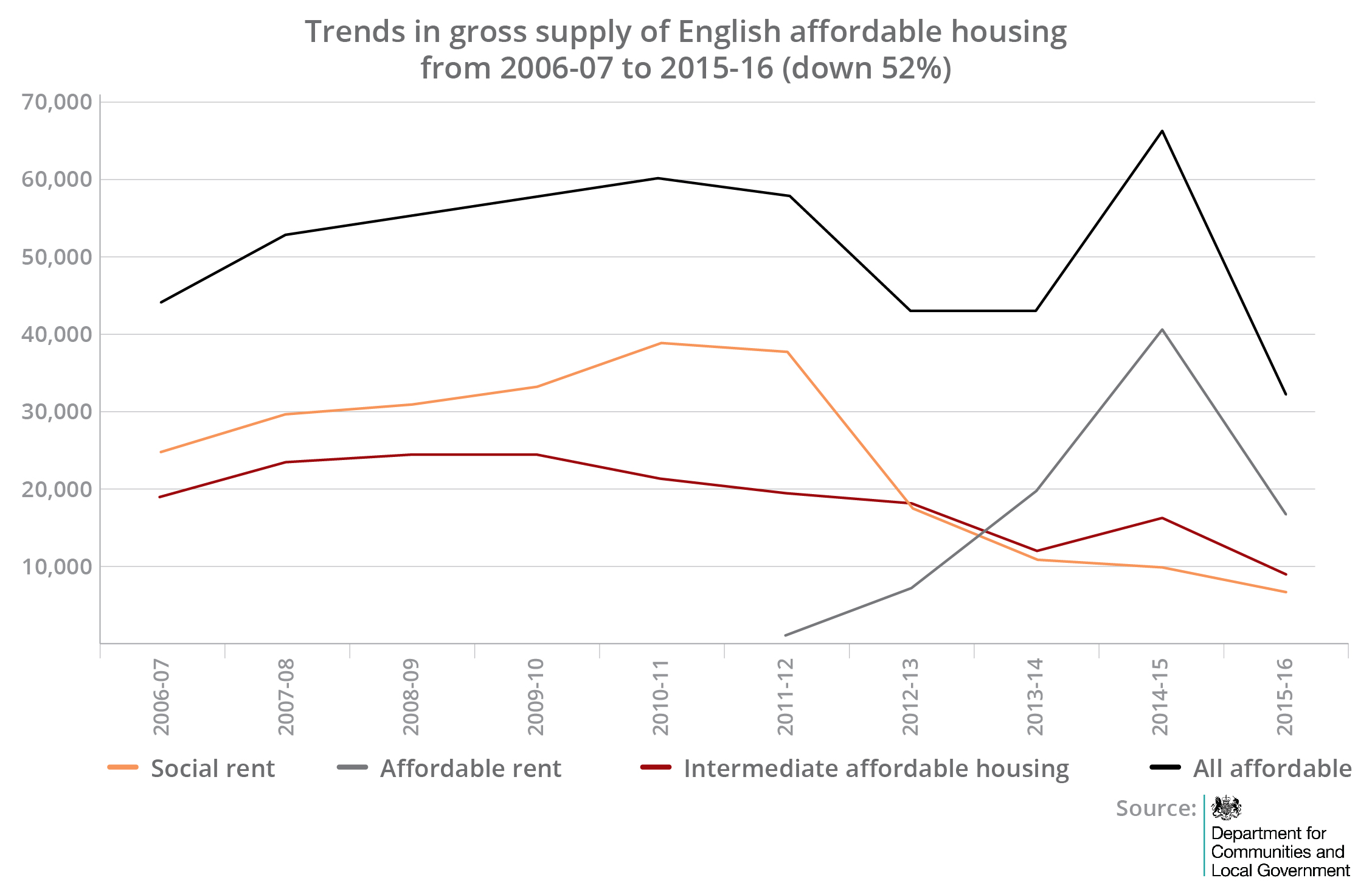

It would fair to assume that much of the property industry was positive about last week´s Autumn Statement, welcoming the range of proposed measures such as the acceleration of housebuilding on public land, relaxing restrictions on grant funding as well as the continuation of right to buy extensions for social tenants and the Help to Buy Equity / ISA schemes. As exemplified by recent DCLG data, in a housing market that is evidently failing to cater to all sections of society, many argued that the government had little choice but to cave into the rising tide of social pressure and support a more universal building cycle.

£1.4 billion will therefore be used to initiate 40,000 housing units by 2020-21 alongside a £2.3 billion fund to deliver infrastructure for up to 100,000 new homes in “areas of high demand”. In addition to plans to rebalance the economy by means of devolving greater power to regional governments, including infrastructure and transport investments in the north, the Chancellor also announced a package of £3.15 billion to deliver over 90,000 units across London. Questions do remain, however, with regards to the mechanics of capital allocation and over the future of Starter Homes provision – both of which are hoped to be addressed in the forthcoming housing white paper (due in January 2017). Nonetheless, the government has demonstrated a clear commitment to expand the delivery of a wider mix of homes for affordable rent, shared ownership and Rent to Buy.

Shortly after the Autumn Statement was an opportune time to speak with David Marshall, Director of Rentplus on this latter form of tenure. A for-profit organisation established in 2013, Rentplus is spearheading the ability for those struggling to save for a deposit and making notable strides in developing its model across the country (see here for some of the pipelined projects). Housing can be accessed by people on council waiting lists, those registered with choice based lettings and Help to Buy agents or those already in private rented accommodation. The “intermediary” model offers renewable Assured Shorthold Tenancies (ASTs) at 5, 10, 15 or 20-year intervals with rents set competitively at 80% of CPI linked open market rates. At the end of each 5-year term (the legal government requirement to benefit from affordable housing status), tenants have an option to buy with a 10% gifted deposit at the point of purchase. By virtue of these longer tenancy terms, Rentplus clients are provided with a greater degree of security alongside a range of benefits of living in a modern home (with a NHBC guarantee and strong energy efficiency performance) and no maintenance, insurance or service charges (where applicable). Encouragingly, David pointed out that their affordable housing units are often built to the same specification as mainstream stock. At purchase, given the fact that tenant-owners are already in situ, there are none of the stresses, uncertainties and other expenses normally associated with moving house.

Rentplus work with Housing Associations (Registered Providers) where properties are leased on a FRI basis. Tenant-owners are encouraged (although not obliged) to view the property as their eventual home, whilst building savings habits and creditworthiness to support future mortgage applications. The extension of the Help to Buy ISA is also expected to supplement future deposit contributions and Rentplus will work with Housing Associations to monitor clients capacity to purchase, providing enough flexibility to ensure that the model caters to a range of financial circumstances.

With a £70 million funding deal with BAE Systems Pension Funds Investment Management and, more recently, a £20 million facility with institutional asset manager Crestline Investors, Rentplus aims to build a minimum of 5,000 affordable homes across England by 2020 through its £4.7 billion Shared Ownership and Affordable Homes Programme (SOAHP). Finance is secured against the properties based on an investment rationale of stable and predictable rental income streams (providing an acceptable running yield by means of inflation-linked coupons) as well as capital returns from the proceeds of a 5-year disposal cycle of 25 percent of aggregated stock. Rentplus will replace properties as they are sold, under the aim of maintaining the number of affordable homes for rent.

David commented that institutional investors generally find the heavily regulated Housing Association environment as attractive, ethical and “bankruptcy remote” with exceptionally low default risks (the sector is also deemed by all of the rating agencies as being of investment grade quality). The Rentplus model was indeed created within the Housing Association environment and on the back of long discussions with the Homes and Community Agency (HCA) as well as Plymouth City Council. The Housing Associations, being the first point of call for tenant-owners, retain an apportioned element of the rent as a management fee in accordance with the agreed Rentplus plan. The properties will be unaffected by policies such Right to Buy (as the properties are not owned by Housing Associations). Time is spent ensuring that partners understand the model and there is sufficient management capacity within each geographical area. Should the properties not be purchased by the occupier after 20 years, they will be sold on the open market with 7.5 percent net proceeds paid to the local authority for future affordable housing.

David continued to explain that Rentplus will be entering into partnerships with developers to purchase affordable homes to be delivered through Section 106 planning agreements under the National Planning Policy Framework (NPPF). The company also intends to jointly procure land with housebuilders and engage in more collaborative involvement with design specifications as early as possible. The challenge here, however, is that some of the large volume builders “commoditise” affordable housing – effectively beholding Rentplus to their own plans. However, with more openness to collaborative partnerships, David argues that builders can unlock funding without the need for grants and meet the necessary planning obligations. Rentplus can further assist house builders in bringing forward stalled sites and alter planning approvals favourably.

I was particularly interested in hearing how the model could be applied across Greater London, considering that just 13,000 affordable units were delivered in the last year, the patent evidence of an ever-widening gulf between house prices and earnings and the blanket “80% of market value” classification being too much of a simplistic view. Whilst Mayor Khan has made a noteworthy commitment to bridging the gap, by means of raising the affordable threshold on schemes to 35% and pledging to deliver 90,000 new affordable home starts by 2020, the task is a mammoth one. Rentplus have been working with the Greater London Authority with a view to making the Rent to Buy model workable in London. Factoring in the London Living Rent (a third of the average household incomes in each borough) and a complex matrix of other issues to surmount, David clarified that the model would be most applicable in the outer “donut” areas and will be dependent on the ability to acquire homes at the right value so the units are genuinely affordable, perhaps complemented by subsidies and grants.

Rentplus certainly is a fascinating model that is comfortably aligned with the mixed-tenure objectives announced by the Chancellor. Institutional backing is likely to mean that scale is more easily achievable compared the bureaucratic and borrowing restraints that invariably characterise Local Authority and Registered Provider development projects. Affordable housing provision can therefore grow sustainably, alleviating the pressures on housing waiting lists, without impacting the public purse. With plans to form a national network of Registered Providers to share best practices, it will be necessary for Councils to effectively implement the model into their Local Plans. The pay-off will be that local authorities can meet their own strategic priorities – stimulating local economies through new jobs and training opportunities. Central government will also have an important role to play in supporting the sector through careful policy making that does not stifle growth. It will certainly be interesting to see how things progress, particularly in speculatively priced parts of London and the South East.