Often referred to as “its own country”, in recent years London´s widening property price gap relative to the rest of the UK has been fuelled by a range of supply-led influences, a historically low interest rate environment and speculatively led exuberance by foreign buyers.

A noticeable peak was observed during the first quarter of 2016 prior to the increased stamp duty obligation on additional property purchases. What followed, however, were clear signs of investors taking a more risk aversive approach in response to what many perceived as a “toppy” marketplace. In addition to the post-Brexit repercussions, that will arguably take some time to filter into the market, the buy to let sector looks set to face its own operational difficulties under stricter regulatory frameworks, higher barriers to entry and the restrictions on mortgage interest tax relief (as a result of the so-called “Alice in Wonderland” policy, initiating from April 2017). There are indeed many reasons for investors to be cautious moving forward. Nonetheless, it is hard to deny that London´s allure as a global economic and cultural hub will continue and below are some key value based principles that PS Investor Services recommend when analysing deals across the Capital:

Picking the Right Areas – a general consensus has emerged that both prices in the City and Inner Parts of London have been undergoing a correction since the latter half of 2015. Whilst opportunities will clearly still exist in these areas, particularly for trading and “added value” projects, investors should certainly monitor ongoing patterns in Outer London and the commuter belts – particularly when considering the wide spectrum of pipelined infrastructure plans already in progress (see this link and click on the interactive map for some prominent examples).

Understanding Price Patterns and Affordability Levels – The best way to analyse local property market fundamentals remains on the ground level carefully considering condition, configuration, type, local area (socio-economic groupings, connectivity, composition, household formation rates, etc.) and a range of other important criteria / idiosyncrasies. Be aware that “price cuts” do not necessarily mean bargains. A narrow comparative sample will usually fail to take into account the heterogeneous nature of London´s housing stock, locational differences as well the 3-month time lag for the most reliable sold house price. We would suggest that investors keep close tabs on Land Registry data via Mouseprice, NetHousePrices and/or Rightmove sold house price data (on the right hand panel of each property listing). “Hands-on” research should also be complemented by reputable data sources (such as the new House Price Index and statistics produced by Acadametrics) alongside platforms and sophisticated datasets such as Insight Residential, Hometrack, Land Insight and Urban Intelligence. Propcision´s “estimated asking price” tool for Rightmove is also useful – although the information should only be used as a rough guideline. Whilst most owner occupiers will be concerned with future capital appreciation prospects, their decisions will invariably be influenced by long-term home ownership as opposed to investment fundamentals. This, conversely, is great if you are selling at the right time.

Focus on Long Term Yield – whilst the outcome of the s. 24 judicial review remains to be seen, portfolio investors would be wise to consider adopting a more professional or “corporatised” expansionary approach (also taking into account future income tax implications of personally owned properties). Our current recommendation is to search for single let properties in good areas across London with a 7%-8% gross yield at purchase, geared conservatively to between 60-70% (assuming that little or no works are required to bring the property into a lettable condition, in which case investors should aim for a higher yield at purchase). Note that this figure will increase when evaluating Houses of Multiple Occupation (HMO) opportunities (i.e. well-developed multi-let / studio accommodation) to factor increased management costs, licencing, voids etc. Readers may be interested in checking the monthly SpareRoom London Rental Index figures to complement their research.

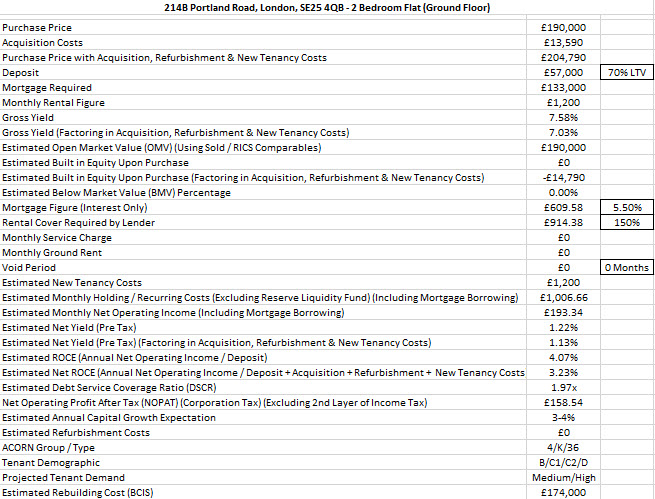

To cite an example, we previously viewed the single-let property below in South Norwood – with good connections to Croydon and approximately 40 minutes travel time to London Bridge. Whilst not the prettiest externally and located on quite a busy road, the flat is modernised to a decent standard with good local amenities:

In and out of auctions and local estate agencies since early 2016, the flat did sell prior to bidding at Auction House London in late July for an undisclosed amount. Below are some headline calculations, assuming the property achieved the guide price and we use an approximate rent of £1,200 per calendar month (unfurnished, based on some rudimentary local research) – producing a relatively healthy gross yield of 7.58%.

Note that the above calculations were made in a “work in progress” spreadsheet (please feel free to critique our analysis via the comments box below or e-mail info@psinvestors.co.uk).

Personally, at £190,000, I still feel the property is overpriced – whether the market moving forward agrees with me is another question! Nonetheless, should parts of Outer London like Croydon become buyers markets in the coming years, opportunities like this with even healthier yields may come to the fore.

It would be prudent for London buy to let investors to take note of the following:

- The rapid growth of the institutionally funded London build to let sector – although unlikely to entirely absorb the huge pent up demand – will certainly raise the bar in terms of accommodation standards and, quite possibly, compress rental yields;

- Rents may not have too much space to grow given reports continue to circulate that charges have increased significantly. There is a growing backlash against periodic rent hikes consuming a disproportionate level of monthly salaries (a recent Radio 4 report entitled “We are so abused as private tenants” – accessible here – attests to the ongoing landlord-tenant tensions, particularly in London);

- It is highly unlikely that Sadiq Khan will implement rent controls – however, the London Mayor´s desire to make the city´s overall housing market more affordable could well have an influence on rental rates.

Beware of the “Below Market Value Illusion” – particularly in a rising market, a closer examination of the facts behind a purported discounted property may lead to disappointing discoveries.

Adding Value Projects – permitted development rights give houses automatic planning consent for a range of modest alterations, from rear extensions to loft conversions, within a set of parameters, effectively bypassing full permission (and the associated costs and time implications). Whilst finding such properties and sites is already becoming competitive and Local Planning Authorities look set to stem the growth of what they deem as “uncontrolled” development, principally by means of the Article 4 direction, the ability to add extra space where possible will certainly pay future dividends both from a yield and long term capital appreciation perspective.

Demographic Changes – whilst being far too premature to predict any kind of exodus from London, should the Brexit negotiation process translate to controlled immigration, certain segments of the tenant market could come under strain. It will be fundamental to continually observe local population growth dynamics and adapt one´s strategy accordingly.

New Build Bargains? An increased amount of recently constructed apartments or units sold by means of assignable contracts have been coming on to the market – suggesting, but not confirming, that early signs of oversupply may be apparent. Nonetheless, an equilibrium point may become apparent as developer´s stall plans in light of the impending Brexit negotiations, rising pressures on build costs and skills shortages. From a yield perspective, London new builds in the current market rarely make sustainable buy to let property investments (unless the purchase is lowly geared).